In his recent article, “Setting the Record Straight on Premium-Financed IUL,” Michael J. Rothman of Succession Capital Alliance argues that premium financing remains a sophisticated estate-planning tool and that its failures reflect only poor execution and disclosure. That defense ignores a deeper problem: The structure itself is unstable. Advocates for the concept argue that “good transactions” mean:

The client has funds to pay the premium out of pocket but chooses to finance.

There is no roll-up of interest on the loan; interest is paid out of pocket.

The death benefit and premium are reasonable relative to income and net worth.

The structure includes full disclosure, meaningful downside stress-testing, and a realistic exit strategy beyond hoping the policy repays the loan.

The policy design is prudent, not maximized for leverage, commissions, or aggressively illustrated returns.

Larry Rybka

I appreciate Michael’s willingness to defend his platform, but his argument overlooks a hard structural and mathematical reality. The widespread failure of these plans is not an execution problem caused by a few bad actors — it is the natural and foreseeable result of an unstable financial design.

My criticism is not of innovative insurance products when they are suitable, well-designed, and sold responsibly. Valmark is proud of its $70 billion in in-force life insurance, and I view life insurance as an important part of my own planning. My criticism is directed at a sales concept that takes an already complex, opaque, and risk-sensitive product and sells it in the most aggressive, highly leveraged way possible. The suggested guardrails above have, in practice, been ignored by both agents and insurers.

Our view at Valmark is informed not only by our review of more than 100 of these plans, including some in litigation. It is also informed by our conclusion, reached 10 years ago when this aggressive sales technique emerged, that premium-financed indexed universal life is not in the client’s best interest. We therefore prohibited the practice by anyone registered at Valmark. The downside was just too great.

A close look at macroeconomic pressures, higher bank loan rates, falling caps and mounting litigation leads to one conclusion: Premium-financed IUL is failing because the math no longer works. And if full disclosure and rigorous suitability were actually applied, the pool of appropriate clients would be vanishingly small.

The death of arbitrage: Real math vs. AG-49 illusions

Premium finance depends on positive arbitrage: Net policy performance must exceed borrowing costs after product charges, loan costs, and commissions. That premise is increasingly unrealistic.

Even after multiple reforms by the National Association of Insurance Commissioners, AG-49 remains an unrealistic baseline as it still permits assumptions that overstate likely outcomes. It is still based on carriers earning 45% on options to credit these policies at the illustrated rate.

Indexing drag: IUL credits exclude dividends, which historically contributed materially to total equity return.

Lower caps: carriers have reduced caps from the mid-teens to roughly 7%–8%, impairing future performance.

Reality: Rothman compares his proposals to a variable universal life policy illustrated at 8%. That flawed comparison is a huge part of the problem. An 8% S&P 500 return can translate to only about 3.82% to 4.30% inside a capped, dividend-free IUL.

Meanwhile, borrowing costs have often risen above 7%. A product earning 4% cannot outpace a loan costing 7%. That turns illustrated arbitrage into negative leverage and has opened massive gaps in collateral.

A special warning for illiquid business owners and real estate clients

The financing pitch often targets business owners and real estate investors with 80% to 90% of net worth tied up in illiquid assets. The argument goes like this: You can earn more money in your business than you can on the policy, so you should borrow to buy your life insurance.

The first part of that premise is true, but the conclusion is flawed. Premium financing compounds the liquidity problem by adding interest-rate, performance and collateral risk. When these programs fail, the collateralized liquid assets outside the business must be tapped or sold at the worst possible time. This is not a risk-management strategy — it is a risk-multiplication trap.

The danger of “zero-return” proprietary indexes

To keep financing going and escape falling S&P 500 caps, promoters have shifted to opaque proprietary indexes marketed with attractive backtests and promises of uncapped returns.

Instead, many have performed worse. During the bull markets of 2023 and 2024, the S&P 500 rose a combined 56%, while many proprietary indexes credited only 1% to 3% and some credited 0%, depending on the index and crediting method.

Under leverage, a single 0% year can turn weak performance into a severe setback, because loan interest keeps compounding even when policy credits do not.

Compounding “debt hole” and the fallacy of patience

When these programs begin to fail, clients are often told to “be patient” and wait for bank rates to fall or performance to improve.

But patience under leverage usually means going deeper into a hole. As cash value lags the compounding loan, the bank demands more collateral.

In jumbo financed cases, clients sign personal notes, borrow millions and pledge liquid assets. In some of Valmark’s second-opinion reviews, required collateral often rises to four to five times the amount originally illustrated.

When liquid assets run out, the bank can call the loan, and the policy can collapse. The downside is not insurance that costs a little bit more — it is financial catastrophe.

The agent’s trap

Agents attracted by large upfront commissions may themselves be walking into a trap. When these structures fail, the damage can flow back to the agents and marketing organizations that sold them through:

Chargeback risk: Lapsed or rescinded financed policies can trigger commission clawbacks of hundreds of thousands of dollars — or more.

The errors and omissions gap: Many E&O policies now exclude premium-financing claims.

This matters because the economic incentives that made these cases attractive at sale may reverse sharply when policies lapse, loans are called or clients pursue recovery.

Systemic litigation shows the concept doesn’t work

Rothman minimizes the industry’s current wave of legal challenges as a “small subset of cases.” The record suggests otherwise. I can identify at least three dozen premium-financed IUL cases in active litigation, several involving multiple policyholders, with many others reportedly settled before filing. The total number is unknowable, and many of these cases are settled before filing through rescission of premium.

The growing wave of lawsuits, class actions and multimillion-dollar judgments is strong evidence that the concept is failing in practice. Courts are increasingly stepping in where state insurance regulation has failed.

Conclusion: Insurance as risk multiplier

Rothman argues that in high net worth estate planning, complexity is not the problem — context is. I disagree. The problem is math: When borrowing costs approach or exceed realistic net policy performance, leverage turns from an estate-planning enhancement into a collateral and liquidity problem.

Not every IUL product is flawed. Used appropriately, with full disclosure and restrained assumptions, IUL can serve a legitimate planning purpose. But premium-financed IUL is different: It layers leverage, collateral risk and optimistic assumptions onto an already complex product.

Traditional life insurance is designed to transfer risk. Premium-financed IUL often does the opposite: It concentrates product risk, credit risk, interest-rate risk, collateral risk and liquidity risk into a single structure.

The concept may survive a little longer in marketing materials. But under realistic math, rising chargebacks and growing litigation, it is not quite dead yet — but close.

That warning is most urgent for business owners and real estate clients with wealth tied up in illiquid assets. What is sold as a way to preserve capital can, at the worst possible time, trigger collateral calls, distressed borrowing or forced sales.

Anyone currently in one of these structures should obtain an independent review now — before loan balances rise further, zero-crediting years compound the shortfall, collateral demands increase or surrender charges make exit options more expensive.

OLDWICK, N.J.–(BUSINESS WIRE)– AM Best has affirmed the Long-Term Issue Credit Rating (Long-Term IR) of “a” (Excellent) on the $846 million (of which $407 million remained outstanding as of March 31, 2026), 6.00% Series Hannover, No. 1 variable funding credit-linked note (Block 1 CLN), due July 1, 2038, issued by Weston2038 LLC (Weston2038), a Delaware limited liability company (issuer). Concurrently, AM Best has affirmed the Long-Term IR of “a” (Excellent) on the $433 million (which upsized to $621 million outstanding as of March 31, 2026), 6.00% Series Hannover, No. 2 variable funding credit-linked note (Block 2 CLN), due July 1, 2043, also issued by Weston2038. The outlook of these Credit Ratings (ratings) is stable.

Both the Block 1 CLN and Block 2 CLN are in consideration of a variable funding surplus note (VSN) issued by Redding Reassurance Company 3 LLC (Redding Re 3), a Missouri-domiciled special purpose financial captive reinsurer and a direct wholly owned subsidiary of Wilton Reassurance Company (Wilton Reassurance). Each VSN supports the excess reserves for a block of life insurance business retroceded by Wilton Reassurance to Redding Re 3 and has a face amount within 100% to 102% of that excess reserve balance. The face amount of the VSN is also equivalent to the face amount of the corresponding credit-linked note for which the VSN is exchanged. For the Block 1 CLN transaction, Wilton Reassurance retrocedes a specified block of level term and universal life secondary guaranty (USLG) business policies on a coinsurance basis to Redding Re 3. For the Block 2 CLN transaction, Wilton Reassurance retrocedes a specified block of USLG business policies oncoinsurance funds withheld basis to Redding Re 3.

The VSN and corresponding credit-linked notes for Block 1 CLN and Block 2 CLN have the same interest rate. Concurrent with the issuance of the credit-linked notes, Weston2038 entered into risk transfer agreements (i.e., cash-settled ISDA swap) with Hannover Life Reassurance Company of America (Bermuda) Ltd. (Hannover Life Re America [Bermuda]) to provide liquidity for any redemption/monetization of the credit-linked notes.

As of December 2025, statutory reserves, economic reserves and excess reserves of the underlying life insurance business pertaining to Block 1 CLN and Block 2 CLN were in line with the projected results.

The rating actions represent AM Best’s current opinion as to the issuer’s ability to meet its financial obligations to the noteholders when due. The ratings primarily take into consideration the following: Hannover Life Re America (Bermuda)’s Long-Term Issuer Credit Rating (Long-Term ICR) of “aa” (Superior) as the swap counterparty to Weston2038; Wilton Reassurance’s Long-Term ICR of “aa-” (Superior), netting arrangements among transaction parties; no reserves or funds at Weston2038, except reliance on funds provided by Redding Re 3; and potential legal risks as it relates to enforceability of the various transaction agreements.

The Long-Term IR could be upgraded or downgraded, and/or the outlook revised if material changes occur in the financial condition and ratings of Hannover Life Re America (Bermuda) or Wilton Re Group, rating unit of which Wilton Reassurance resides.

This press release relates to Credit Ratings that have been published on AM Best’s website. For all rating information relating to the release and pertinent disclosures, including details of the office responsible for issuing each of the individual ratings referenced in this release, please see AM Best’s Recent Rating Activity web page. For additional information regarding the use and limitations of Credit Rating opinions, please view Guide to Best’s Credit Ratings. For information on the proper use of Best’s Credit Ratings, Best’s Performance Assessments, Best’s Preliminary Credit Assessments and AM Best press releases, please view Guide to Proper Use of Best’s Ratings & Assessments.

AM Best is a global credit rating agency, news publisher and data analytics provider specializing in the insurance industry. Headquartered in the United States, the company does business in over 100 countries with regional offices in London, Amsterdam, Dubai, Hong Kong, Singapore and Mexico City. For more information, visit www.ambest.com.

Shares of Globe Life Inc. (NYSE: GL) traded at a new 52-week high today and are currently trading at $164.64. So far today, approximately 38,719 shares have been exchanged, as compared to an average 30-day volume of 569.68k shares.

Globe Life Inc. delivers diverse life insurance and supplementary health coverage, alongside annuity products, targeting households in the lower-middle to middle-income brackets throughout the United States. The company’s operations are structured into four key segments: Life Insurance, Supplemental Health Insurance, Annuities, and Investments. Its offerings encompass whole life, term life, and other life protection plans and supplemental health benefits like Medicare supplements.

Globe Life Inc. share prices have moved between a 52-week high of $164.79 and a 52-week low of $116.73. The stock has moved 2.1% over the past week.

IBN consists of financial brands introduced to the investment public over the course of 20+ years. With IBN, we have amassed a collective audience of millions of social media followers. These distinctive investor brands aim to fulfill the unique needs of a growing base of client-partners. IBN will continue to expand our branded network of highly influential properties, leveraging the knowledge and energy of specialized teams of experts to serve our increasingly diversified list of clients.

Please see full terms of use and disclaimers on the InvestorBrandNetwork website applicable to all content provided by IBN, wherever published or re-published: http://IBN.fm/Disclaimer

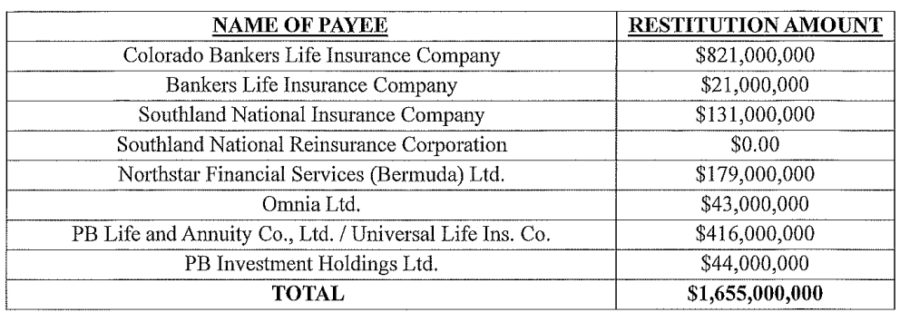

Greg Lindberg is asking a federal court to halt ongoing asset sales tied to a $1.655 billion restitution order, arguing that a proper accounting under federal restitution law shows he owes nothing.

In fact, Lindberg claims he overpaid by about $1.27 billion.

On May 28, District Judge Max O. Cogburn accepted the report of the special master and ordered Lindberg to pay restitution of $1.655 billion. Cogburn ordered the following restitution amounts to the life insurance and other companies once owned by Lindberg.

Cogburn’s order declares the amount “due and payable immediately.” The order is enforceable as a federal judgment and authorizes liens against Lindberg’s property.

In a motion filed Tuesday, Lindberg challenged the restitution order and sought to prevent further liquidation of his assets while the dispute is resolved.

Lindberg has not responded to repeated inquiries from InsuranceNewsNet.

Lindberg and his co-conspirators caused companies he controlled in North Carolina, Bermuda, Malta, and elsewhere to invest more than $2 billion in loans and other securities with his own affiliated companies and laundered the proceeds of the scheme, the government has said.

Lindberg directed the scheme and personally benefitted from the fraud in part by “forgiving” more than $125 million in loans to himself from the insurance companies that he controlled. Lindberg used his ill-gotten gains to fund a lavish lifestyle, buying private jets, mansions and a 200-foot luxury yacht, court documents say.

Exceeded the recommendation

While Cogburn accepted the arguments put forth by the special master, attorney Joseph Grier of the law firm Grier Wright Martinez PA, his order increased the restitution amount by $30 million. Grier’s report proposed a restitution figure of approximately $1.625 billion.

Lindberg’s attorneys contend that Cogburn acted before fully considering the objections filed by the defense. In a memorandum accompanying the stay request, they argue that mandatory offsets totaling nearly $2.9 billion reduce the restitution obligation to zero and show an overpayment of roughly $1.24 billion.

According to the filing, the offsets are supported by pleadings from restitution recipients, business records, and legal precedent governing restitution calculations under the federal Mandatory Victims Restitution Act.

Continuing to sell Lindberg’s assets while the restitution calculation remains disputed would improperly allow recovery beyond any actual losses suffered by victims, the memo argues. The filing cites federal appellate and Supreme Court decisions that limit restitution awards to actual losses and require a causal connection between a defendant’s conduct and claimed damages.

“The relief Mr. Lindberg seeks is also necessary to prevent further destruction of the assets that, on the present record, the Court is being asked to liquidate to fund a phantom restitution obligation,” the memo argues.

Poor investment decisions alleged

The defense also argues that assets currently being liquidated have declined in value because of decisions made during insurance rehabilitation proceedings that followed Lindberg’s removal from control of affiliated companies.

According to the filing, companies associated with Lindberg grew to an estimated enterprise value of $3.4 billion during his ownership and generated more than $300 million in annual earnings.

The motion contrasts that performance with the results achieved under rehabilitation, alleging that more than $165 million was paid in fees, $137 million was lost through bond portfolio decisions and several potential transactions that could have generated substantial proceeds were rejected.

The filing points to a 2018 letter of intent from alternative asset manager Ares Management and a 2019 proposal from Oaktree Capital Management as evidence that potential transactions existed that could have provided sufficient funds to satisfy policyholder obligations. Lindberg’s attorneys argue that decisions to reject those transactions broke any chain of causation linking subsequent losses to Lindberg’s conduct.

The motion seeks three forms of relief:

First, Lindberg asks the court to stay further asset sales until it rules on his objections to the restitution calculation.

Second, he seeks the return of what the filing describes as “Primary Restitution Assets,” arguing that restitution has already been fully satisfied.

Third, as an alternative, Lindberg requests the return of eight smaller affiliated companies that court filings have previously described as having no material value to the rehabilitation estates and not being slated for sale.

Freedom Lifetime CITs will combine target date investing with lifetime income options from Nationwide® and New York Life®, aiming to help many Americans retire with greater confidence

BOSTON–(BUSINESS WIRE)–

Target-date pioneer and industry leaderi Fidelity Investments® today announced plans to launch Fidelity Freedom® Lifetime, a suite of target date collective investment trusts (CITs) with a built-in guaranteed income option*. This retirement solution will be available to employers and plan sponsors on Fidelity’s recordkeeping platform in early 2027.

Freedom Lifetime will leverage Fidelity’s time-tested target date strategy that has helped millions of Americans save for retirement for more than 30 yearsi, combined with the option to convert a portion of an employee’s target date balance into guaranteed lifetime income*. The Freedom Lifetime suite will include a strategic allocation to an insurance pool through Nationwide and New York Life— two highly rated insurers with deep expertise in delivering guaranteed income solutionsii. This exposure will allow employees participating in employer retirement plans, particularly those nearing and in retirement, to elect to receive a guaranteed lifetime income stream* designed to create predictable income throughout retirement.

“Increasingly, employees are looking for more clarity in their retirement income streams,” said Molly Cunningham, head of Workplace Lifetime Financial Help. “In designing Freedom Lifetime, our priority was to maximize the value of lifetime income while keeping the participant and plan sponsor experience simple and easy to adopt. Along with Fidelity’s deep target date and asset management expertise, employees can benefit from Fidelity’s integrated and holistic support including education, tools, and dedicated live, one‑on‑one support to help employees create a retirement plan that fits their goals.”

“Nationwide is pleased to extend our strong ongoing relationship with Fidelity by serving as an insurer on Fidelity Freedom Lifetime, which marks an important step forward in expanding access to retirement income solutions for America’s workers,” said Kevin Jestice, president of Retirement Solutions at Nationwide. “As a protection company with 100 years of experience safeguarding people and businesses, and more than a decade of experience with lifetime income solutions specifically designed for use within employer-sponsored retirement plans, we’ve seen how essential these offerings are as more employees approach retirement and look to turn savings into dependable income for a dignified retirement.”

“For more than 180 years, New York Life has helped individuals turn savings into lasting financial security,” said David Cruz, head of Institutional Annuities at New York Life. “As the largest mutual life insurance company in the U.S.iii, we’re proud to bring our deep expertise in guaranteed income solutions to Fidelity Freedom Lifetime, an important step in expanding access to retirement income for employees. With our long-term focus and experience delivering income for life, we are excited about this opportunity to help employees turn their savings into income that they can depend on throughout retirement.”

Freedom Lifetime will utilize a blended investment approach, investing in a mix of active and index underlying funds, including the insurance pool, while employing active asset allocation across different asset classes. The series will offer competitive pricing, with asset-based pricing dependent on share class and vintage. The portfolio management team for Freedom Lifetime will include long-tenured target date co-portfolio managers Andrew Dierdorf, Brett Sumsion, Finola McGuire Foley, and Cait Dourney Earle, who collectively have more than 85 years of experience at Fidelity and are grounded in the firm’s unparalleled global research organization.

“Fidelity’s deep research and capital‑markets expertise allow us to build the diversified Freedom Lifetime portfolios that are paired with the purposeful design of meeting predictable income needs,” said Andrew Dierdorf, co-portfolio manager of the Fidelity Freedom Lifetime Suite. “This offering provides access to guaranteed income to help keep employees on track toward their retirement goals.”

Employees will also have access to a digital experience that is fully integrated through Fidelity’s record-keeping platform. This experience will provide users with the ability to model scenarios to illustrate potential income in retirement and, when eligible to purchase lifetime income, obtain real-time guaranteed income quotes, which allows them to take action to convert a portion of savings into lifetime income.

Fidelity’s Retirement Income Products and Solutions

As a leading workplace benefits provider, Fidelity offers a variety of options designed to help employees better manage the transition from saving for retirement to living in retirement, which includes retirement investment selections, flexible withdrawal strategies, and managed account and guaranteed income solutions. In 2024, Fidelity introduced Guaranteed Income Direct, a new solution allowing employees to convert all or a portion of their retirement savings – from a 401(k), 403(b) or 457(b) – into an immediate income annuity to provide consistent, pension-like payments throughout retirement.

Fidelity’s Target Date Platform

Fidelity helps more Americans with retirement than any other companyiv and its target date solutions are designed to help investors grow their retirement savings during their earning years while also helping to provide income and stability through their retirement years. Fidelity offers a range of active, index and blend target date solutions totaling more than $770 billion in assetsvi. To learn more about Freedom Lifetime, visit https://www.fidelityworkplace.com/s/freedom-lifetime.

About Fidelity Investments

Fidelity’s goal is to strengthen the financial well-being of our customers and deliver better outcomes for the clients and businesses we serve. Fidelity’s strength comes from the scale of our diversified, market-leading financial services businesses that serve individuals, families, employers, wealth management firms, and institutions. With assets under administration of $17.9 trillion, including managed assets of $7.0 trillion as of March 31, 2026, we focus on meeting the unique needs of a broad and growing customer base. Privately held for 79 years, Fidelity employs more than 80,000 associates across North America, Europe, and Asia-Pacific. For more information about Fidelity Investments, visit https://www.fidelity.com/about-fidelity/our-company.

About Nationwide

Nationwide, a Fortune 100 company based in Columbus, Ohio, is one of the largest and strongest diversified financial services and insurance organizations in the United States. Nationwide is rated A+ by Standard & Poor’s. An industry leader in driving customer-focused innovation, Nationwide provides a full range of insurance and financial services products including auto, business, homeowners, farm and life insurance; public and private sector retirement plans, annuities and mutual funds; excess & surplus, specialty and surety; and pet, motorcycle and boat insurance.

For more information about Nationwide and Nationwide’s ratings, visit www.nationwide.com or Company Ratings — Nationwide.

New York Life Insurance Company (www.newyorklife.com), a Fortune 100 company founded in 1845, is the largestiii mutual life insurance company in the United States and one of the largest life insurers in the world. Headquartered in New York City, New York Life’s family of companies offers life insurance, disability income insurance, retirement income, investments, and long-term care insurance. New York Life has the highest financial strength ratings currently awarded to any U.S. life insurer from all four of the major credit rating agencies.v

Investing involves risk, including risk of loss.

Unless otherwise expressly disclosed to you in writing, the information provided in this material is for educational purposes only. Any viewpoints expressed by Fidelity are not intended to be used as a primary basis for your investment decisions, are based on facts and circumstances at the point in time they are made, and are not individualized or particularized to you, your plan, or your plan’s participants or beneficiaries. Accordingly, Fidelity and its representatives are not acting in a fiduciary capacity, and nothing in this material constitutes impartial investment advice, under or within the meaning of the Employee Retirement Income Security Act of 1974 or the Internal Revenue Code of 1986, both as amended, or any regulations or other guidance thereunder. Fidelity and its representatives may have a conflict of interest in the products or services mentioned in this material because they have a financial interest in the products or services and may receive compensation, directly or indirectly, in connection with the management, distribution, and/or servicing of these products or services, including Fidelity funds, certain third-party funds and products, and certain investment services.

No target date investment option is considered a complete retirement program and there is no guarantee any single investment option will provide sufficient retirement income at or through retirement. Principal invested is not guaranteed at any time, including at or after the pools’ target dates. In order to provide an income stream, there is no or limited access to assets rolled over to purchase individual retirement annuities from the Insurers. Annuity guarantees are subject to the claims-paying ability of the issuing insurance company. Investment performance of the Fidelity Freedom Commingled Pool products depends on the performance of the underlying investment options and on the proportion of the assets invested in each underlying investment option. The investment risk of each Fidelity Freedom Commingled Pool changes over time as its asset allocation changes. These risks are subject to the asset allocation decisions of the portfolio manager. Pursuant to Fidelity Institutional Asset Management Trust Company’s (the Adviser) ability to use an active asset allocation strategy, investors may be subject to a different risk profile compared to the commingled pool’s strategic asset allocation strategy shown in its glide path. The commingled pools are subject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad, and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities. Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. The Adviser may buy and sell futures contracts (both long and short positions) in a commingled pool in an effort to manage cash flows efficiently, remain fully invested, or facilitate asset allocation.

*Certain Fidelity Freedom Lifetime collective investment trusts (CITs) include allocations to group annuity contracts issued to Fidelity Institutional Asset Management Trust Company by the insurers during accumulation. This annuity allocation provides plan participants with the option to elect to receive guaranteed lifetime income at retirement age from selected insurers through the purchase of rollover individual retirement annuities. Both the group annuity and individual annuity contracts are subject to the claims paying ability of the issuing insurers.

Any rollover individual retirement annuity is opened directly with each insurer pursuant to their respective new account opening procedures. Assets used to purchase the income stream will no longer be liquid.

This investment option may not be available in all states or territories.

Neither FIAM nor FIAM TC (“Fidelity”) are insurance companies and make no guarantees as to the contractual obligations of each insurer. Insurers are not affiliated with each other or with Fidelity and its affiliates.

The Fidelity® Freedom Lifetime Commingled Pools are commingled pools of the FIAM Group Trust for Employee Benefit Plans, and are managed by Fidelity Institutional Asset Management Trust Company (FIAM TC), a trust company organized under the laws of the State of New Hampshire.

The Fidelity® Freedom Lifetime Commingled Pool is not a mutual fund.

Fidelity Institutional Asset Management (FIAM) includes the following entities that provide investment services FIAM TC and FIAM LLC, a U.S. registered investment adviser. Fidelity Asset Management Solutions (FAMS) provides a broad array of investment solutions with its Global Institutional Solutions (GIS), Global Asset Allocation (GAA), and institutional equity, fixed income, high income, and alternative asset management teams through FIAM LLC, FIAM TC and Fidelity Diversifying Solutions LLC.

FIAM products and services may be presented by Fidelity Distributors Company LLC, Fidelity Institutional Wealth Adviser LLC, or Fidelity Brokerage Services, LLC, Member NYSE, SIPC, each a non-exclusive financial intermediary that is affiliated with FIAM, or Fidelity Investments Canada ULC and FIL Limited, all of which are compensated for such services.

Certain data and other information in this report were supplied by outside sources and are believed to be reliable and current. However, Fidelity cannot verify the accuracy of such information, and such information is subject to change without notice.

Fixed annuities available through Guaranteed Income Direct are issued by third-party insurance companies, which are not affiliated with any Fidelity Investments company. A contract’s financial guarantees are solely the responsibility of and are subject to the claims-paying ability of the issuing insurance company.

Income annuities available as plan distribution options are selected by the plan’s fiduciaries and sold and issued by third-party insurance companies which are not affiliated with any Fidelity Investments company. Fidelity Health Insurance Services, LLC (“FHIS”) may receive a fee from the issuing insurance company; however, FHIS does not directly or indirectly solicit, negotiate, or sell any annuities available as plan distribution options. A contract’s financial guarantees are solely the responsibility of and are subject to the claims paying ability of the issuing insurance company.

Pension benefits are guaranteed by the plan sponsor unless the sponsor transfers the liability to a third-party insurance company. Unlike pensions, annuities must be purchased and have associated costs and expenses.

The third parties mentioned herein and Fidelity Investments are independent entities and are not legally affiliated.

A link to third-party material is included for your convenience. The content owner is not affiliated with Fidelity and is solely responsible for the information and services it provides. Fidelity disclaims any liability arising from your use of such information or services. Review the new site’s terms, conditions, and privacy policy, as they will be different from those of Fidelity’s sites.

Fidelity Health Insurance Services, LLC

245 Summer Street, V4C, Boston, MA 02210-1129

Fidelity Brokerage Services LLC, Member NYSE, SIPC

900 Salem Street, Smithfield, RI 02917

Fidelity Distributors Company LLC

900 Salem Street, Smithfield, RI 02917

National Financial Services LLC, Member NYSE, SIPC

i Fidelity’s Freedom Funds are an industry-leading target date strategy based on AUM market share of the target date fund industry at #2 overall target date and #1 blend target date share, according to U.S.-based target date retirement assets under management (mutual fund + CIT) as of CY 2025, Sway Research. Fidelity has over 30 years of target date experience and innovation, with over $770B in AUM as of 12/31/2025 and 18k plan sponsor clients and 7m+ in shareholders invested – shareholders include DC (including TEM) participants and retail investors on Fidelity’s platform only, based on Fidelity internal analysis, as of 06/30/2025.

ii Nationwide and New York Life are two experienced, and highly rated insurers based on their stability, claims-paying ability and overall financial strength: Nationwide Life Insurance Company, with over 100 years’ experience, is rated A+ by S&P Global ratings, the fifth highest of 21 ratings. Affirmed: 04/12/25. New York Life Insurance Company and New York Life Insurance and Annuity Corporation, with over 180 years’ experience, has received the highest financial strength ratings currently awarded to any U.S. life insurer by A.M. Best (A++), Fitch (AAA), Moody’s (Aa1), and Standard & Poor’s (AA+). Source: Individual Third-Party Ratings Reports as of 9/30/25. There is no guarantee that current ratings will be maintained.

iii Based on revenue reported by Fortune 500 ranked within Industries – Insurance: Life, Health (Mutual), Fortune Magazine, June 3, 2025. For methodology, please visit https://fortune.com/ranking/fortune500/2025/#methodology.

v Individual independent rating agency commentary as of 10/28/2025: A.M. Best (A++), Fitch (AAA), Moody’s Investors Service (Aa1), Standard & Poor’s (AA+).

NEW YORK–(BUSINESS WIRE)–

KBRA releases commentary following the recent publication of the Columbia Business School’s Rating Without Market Discipline paper, which raises important questions regarding the growth of private ratings in U.S. life insurer portfolios and the interaction between ratings and regulatory capital. The paper concludes that privately rated bonds understate credit risk, experience higher subsequent impairment rates, and contribute to lower required capital than comparable publicly rated bonds.

This KBRA research reviews the paper’s methodology and its interpretation of the evidence. Our objective is not to argue that private ratings should be exempt from scrutiny. Rather, it is to help fixed income investors evaluate whether the evidence presented in the paper supports the breadth of its conclusions—which, we believe, they do not. Put differently, the paper’s rhetorical emphasis is on systemic risk, policyholder welfare, widespread rating inflation, and the absence of market discipline, while its principal quantitative estimate is a hypothetical modeled capital adjustment that is insignificant relative to the financial resources of the industry.

Key Takeaways

Even if one accepts the entirety of the paper’s analytical assumptions and inferential steps as valid, the authors’ own illustrative capital exercise implies approximately $4 billion of additional required capital for the entire U.S. life insurance industry.

Based on NAIC’s 2024 Life RBC Statistics, that amount represents roughly 0.5% of industry total adjusted capital (TAC), approximately 0.6% of industry surplus, and less than 0.1% of invested assets. In other words, a small pro forma impact on the industry’s risk-based capital ratio (RBC) of approximately 38 RBC points (830% versus 868%).

That conclusion is considerably narrower and economically more modest than the impression conveyed by the paper’s title, abstract, and concluding discussion.

KBRA, one of the major credit rating agencies, is registered in the U.S., EU, and the UK. KBRA is recognized as a Qualified Rating Agency in Taiwan, and is also a Designated Rating Organization for structured finance ratings in Canada. As a full-service credit rating agency, investors can use KBRA ratings for regulatory capital purposes in multiple jurisdictions.

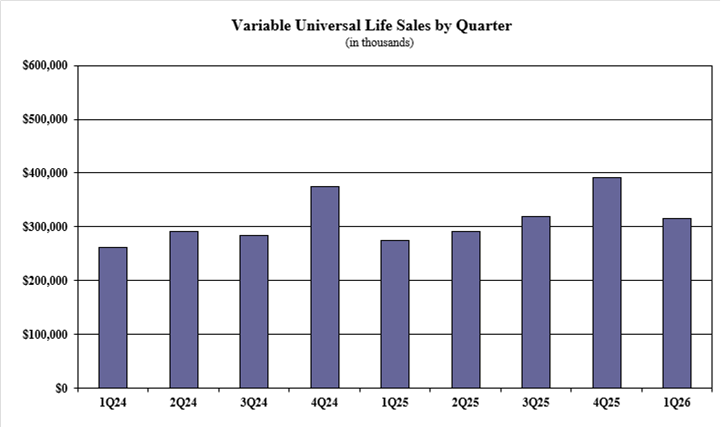

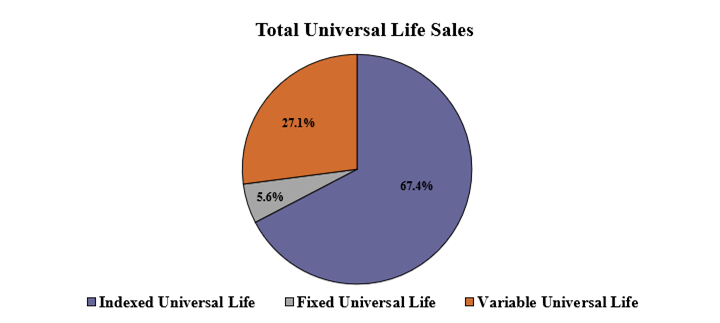

Variable universal life insurance is known for the flexibility it offers clients. According to first-quarter sales numbers from Wink, Inc., clients are embracing the product.

VUL sales were up 15.1% over Q1 2025, Wink reported in its latest Sales & Market Report. Sales began percolating during the fourth quarter, with VUL up 4.3% over the prior-year quarter and up 22.4% over Q3.

Sales are slowest during Q1 and strongest at the end of the year. Total VUL sales for the first quarter were $316.1 million, down 19.1% quarter-over-quarter.

“The market has been on the uptick since the beginning of April,” said Sheryl Moore, CEO of Wink, Inc. and Moore Market Intelligence. “This translates to improved sales of variable UL.”

VUL is a permanent life insurance policy that combines a death benefit with an investment component. Policies can be customized with specific riders to provide coverage for needs such as long-term care.

Items of interest in the VUL market included Prudential retaining the No. 1 ranking in sales, with a 36.2% market share; Pacific Life Companies, Nationwide, RiverSource Life and John Hancock completed the top five, respectively.

Pruco Life’s PruLife Custom Premier II was the No. 1 selling VUL product, for all channels combined, for the quarter. The top primary pricing objective for sales this quarter was cash accumulation, capturing 63.4% of sales. The average VUL target premium for the quarter was $23,161, a decline of nearly 10% from the prior quarter.

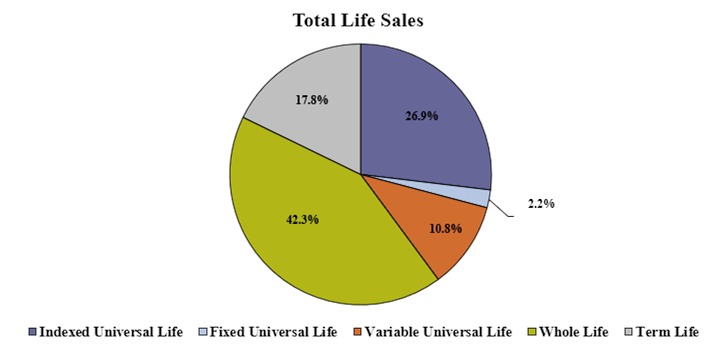

Overall life sales up 8%

All life insurance sales for the first quarter were more than $2.9 billion, down 9.7% compared to the previous quarter and up 8.1% compared to the same period last year. All life sales include fixed universal life, indexed UL, variable UL, indexed whole life, whole life and term life product sales.

Noteworthy highlights for total life insurance sales of all products in the first quarter included Prudential ranking as No. 1 in overall sales for all life insurance sales, with a market share of 5.6%. Americo’s Eagle Select, a whole life product, was the No. 1 selling product for all life insurance sales, for all channels combined, for the quarter.

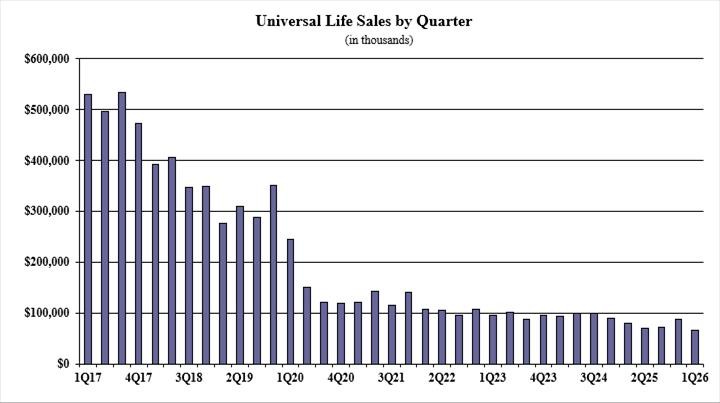

All universal life sales for the first quarter were $1.1 billion, down 16% compared to the previous quarter and up 4.3% compared to the same period last year. All universal life sales include fixed UL, indexed UL and variable UL product sales.

Noteworthy highlights for all universal life sales in the first quarter included Prudential ranking as No. 1 in overall sales for all universal life products, with a market share of 11.2%. Life Insurance Co. of the Southwest’s FlexLife, an indexed universal life product, was the No. 1 selling product for all universal life sales, for all channels combined, for the quarter.

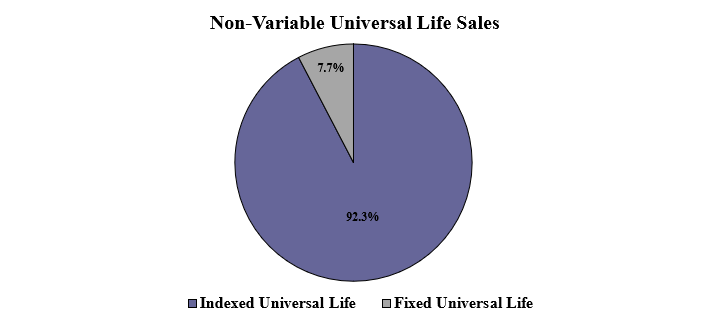

Non-variable universal life sales for the first quarter were $851.9 million, down 15.2% when compared to the previous quarter and up less than 1% compared to the same period last year. Non-variable universal life sales include both fixed UL and indexed UL product sales.

Noteworthy highlights for total non-variable universal life sales in the first quarter included National Life Group retaining the No. 1 overall sales ranking for non-variable universal life sales, with a market share of 13.8%. Life Insurance Co. of the Southwest’s FlexLife, an indexed universal life product, was the No. 1 selling product for non-variable universal life sales, for all channels combined, for the quarter.

Fixed universal life sales for the first quarter were $65.2 million, down 25.9% compared to the previous quarter and down 18% compared to the same period last year.

Items of interest in the fixed UL market included Nationwide retaining its No. 1 ranking in fixed universal life sales, with a 22.8% market share; Pacific Life Companies, John Hancock, Protective Life Companies and Penn Mutual completed the top five, respectively.

Nationwide’s Nationwide CareMatters II was the No. 1 selling fixed universal life insurance product, for all channels combined, for the quarter. The top primary pricing objective of no lapse guarantee captured 33.0% of sales. The average fixed UL target premium for the quarter was $6,826, a decline of more than 22% from the prior quarter.

“Universal life sales have never been this low,” Moore said. “It is just getting more difficult to justify the sales of these products, when indexed life has a relatively stronger value proposition.”

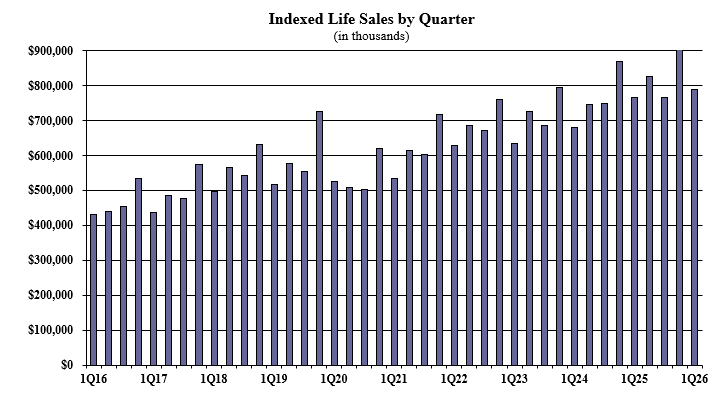

Indexed life sales for the first quarter were $789.5 million, down 14% compared with the previous quarter, and up 2.8% compared to the same period last year. Indexed life sales include both indexed UL and indexed whole life.

Items of interest in the indexed life market included National Life Group retaining its No. 1 ranking in indexed life sales, with a 14.7% market share; Pacific Life Companies, John Hancock, Nationwide, and Fidelity and Guaranty Life rounded out the top five, respectively.

Life Insurance Co. of the Southwest’s FlexLife was the No. 1 selling indexed life insurance product, for all channels combined, for the quarter. The top primary pricing objective for sales in the quarter was cash accumulation, capturing 74.7% of sales. The average indexed life target premium for the quarter was $12,922, a decline of nearly 3% from the prior quarter.

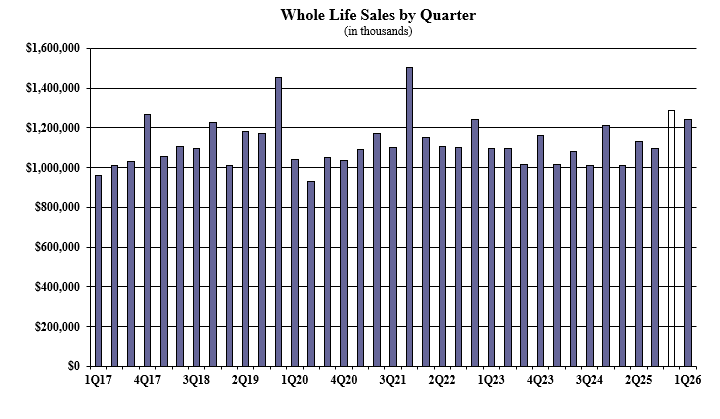

Whole life first quarter sales were over $1.2 billion, down 3.6% compared with the previous quarter, and up 22.6% compared to the same period last year. Items of interest in the whole life market included the top primary pricing objective of final expense, capturing 72.4% of sales. The average premium per whole life policy for the quarter was $3,860, a decline of more than 19% from the prior quarter.

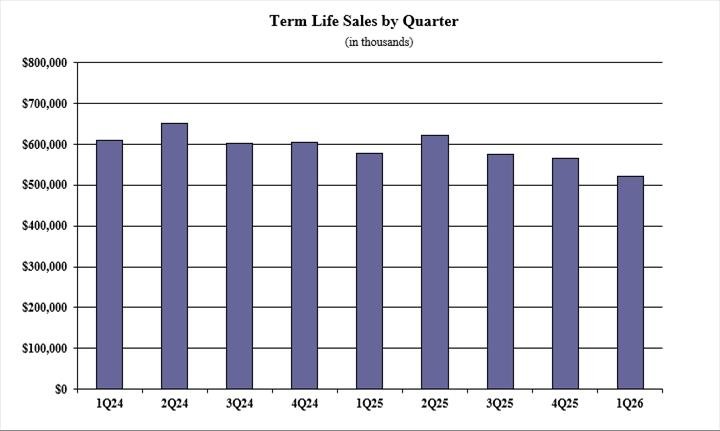

Term life first-quarter sales were $521.8 million, down 7.6% when compared with the previous quarter and down 9.7% compared to the same period last year.

Items of interest in the term life market include Prudential ranking as No. 1 in term life sales, with a 6.5% market share. Pacific Life Companies, Protective Life Companies, Corebridge Financial, and National Life Group completed the top five, respectively.

Protective Life Classic Choice Term 20 was the No. 1 selling term life insurance product, for all channels combined, for the quarter. The average annual term life premium per policy reported for the quarter was $1,905, a decline of nearly 29% from the previous quarter.

Wink now reports sales on all annuity lines of business, as well as all life insurance product lines.

Rate enhancements also made to flagship traditional variable annuity product suite

LANSING, Mich.–(BUSINESS WIRE)– Jackson National Life Insurance Company® (Jackson®), the main operating subsidiary of Jackson Financial Inc.1 (NYSE: JXN), today launched Jackson Market Link Pro® 4 (JMLP4) and Jackson Market Link Pro Advisory® 4 (JMLPA4), further strengthening Jackson’s suite of registered index-linked annuities (RILAs). JMLP4 (commission-based) and JMLPA4 (fee-based) provide clients the potential to grow assets before and during retirement while offering different degrees of protection, including full principal protection, against unexpected market events. Additionally, Jackson recently made improvements to its flagship traditional variable annuity (VA) product suite, delivering enhanced value and flexibility to financial professionals and their clients.

“Jackson continues our focus on expanding retirement planning options for financial professionals and their clients with these enhancements to our RILA and traditional VA product suites,” said Alison Reed, EVP, Head of Distribution, Jackson National Life Distributors LLC (JNLD), the marketing and distribution business of Jackson. “By being the first in the industry to introduce the Dow Jones Industrial Average (DJIA) as an index option with a RILA, offering clients the ability to add funds to an existing contract and adding a guaranteed cap crediting method that locks in rates for six premium years, we’re empowering clients with more choice and confidence in their investment strategies.”

JMLP4 and JMLPA4 enhancements include the following:

DJIA Index Option: The addition of the DJIA as an index option provides clients with another avenue to invest their funds in accordance with their unique values and investment preferences and is now available alongside the S&P 500, Russell 2000, Nasdaq-100, MSCI EAFE and MSCI Emerging Markets. Jackson will not restrict which index options can be selected with each crediting method or protection option, enabling clients to adjust their allocations without triggering unwanted tax consequences and invest in what aligns with their priorities2.

Flexible Premiums: JMLP4 and JMLPA4 are the first RILA products offered at Jackson designed to allow flexible premiums. This feature allows clients to add funds to an existing contract without submitting a new application, providing a more streamlined and convenient way to invest additional assets.

Guaranteed Cap Crediting Method3: Clients can lock in a cap rate removing any concern with what the renewal rate will be for the entire guarantee period, which is the first six premium years. This feature is only available on the 1- and 3-year terms with a 10% buffer.

Full or Partial Performance Lock: With a performance lock, clients can choose to lock in all (full performance lock) or a portion (partial performance lock) of their interim value at any point during the index account option term. In practice, the value at the lock-in point moves to a performance lock holding account where amounts earn a declared rate of interest until the next premium allocation anniversary4, when it can be reallocated.

Rate Enhancement Option5: At contract issue, for an additional charge, consumers can elect a rate enhancement option on all available terms, crediting methods, and protection options, providing the opportunity for greater growth.

In addition to these enhancements, Jackson’s JMLP RILA suite offers the following competitive features:

Full Principal Protection: The JMLP4 suite offers a 100% buffer (30% buffer in New York) protection option for the 1-year cap, 3-year cap, 6-year cap and 1-year performance trigger crediting methods, in addition to 10% and 20% options. The level of protection depends on the crediting method selected6.

Flexible Index Account Option Terms: Jackson offers 1-year, 3-year and 6-year index account option terms7. Any gains or losses in the tracked index(es) (described above) are calculated at the end of the term, and the contract value is adjusted accordingly.

Multiple Crediting Methods: Jackson offers a diverse menu of crediting methods that allows consumers the ability to customize their contract both in terms of growth potential and protection level. In addition to the guaranteed cap crediting method, Jackson offers three additional crediting methods – cap, performance boost8 and performance trigger.

Enhancements to Extended Care9 and Terminal Illness10 Waivers: Beginning with JMLP4, there is no limit on the frequency of withdrawals that can be made utilizing these waivers and no cap on the amount of money that can be withdrawn.

Legacy and Cost Control: Through the built-in death benefit11 — available at no additional charge — clients can help protect their retirement assets against market downturns while providing a legacy for beneficiaries. Additionally, with no annual contract fees12, more investable assets remain in clients’ contracts.

Jackson also recently announced the following enhancement to its suite of VAs as well as a series of fund changes.

Guaranteed Withdrawal Rates: Jackson has increased Single Life and Joint Life Guaranteed Annual Withdrawal Amount Percentages (GAWA%) across multiple options within its Flex Suite of living benefits and New York Flex Suite of living benefit options, including Flex Core, Flex Net Core, Flex DB Core, and Flex Plus.

“As market conditions and client needs continue to evolve, Jackson is enhancing our industry leading variable annuity lineup to provide financial professionals and their clients with more options and flexibility,” said Brian Sward, EVP, Head of Product Solutions, JNLD. “These enhancements reinforce our commitment to delivering value across a broad range of market environments and reflect Jackson’s ongoing dedication to providing products that support personalized strategies and long-term financial success.”

Financial professionals who would like to learn more about Jackson’s recent product enhancements can contact the company at 1-800-711-7397, connect with their local wholesaler or visit http://www.jackson.com/financial-professional.

ABOUT JACKSON

Jackson® (NYSE: JXN) is committed to helping clarify the complexity of retirement planning—for financial professionals and their clients. Through our range of annuity products, financial know-how, history of award-winning service* and streamlined experiences, we strive to reduce the confusion that complicates retirement planning. We take a balanced, long-term approach to responsibly serving all our stakeholders, including customers, shareholders, distribution partners, employees, regulators and community partners. We believe by providing clarity for all today, we can help drive better outcomes for tomorrow. For more information, visit www.jackson.com.

*SQM (Service Quality Measurement Group) Call Center Awards Program for 2004 and 2006-2025. (Criteria used for Call Center World Class FCR Certification is 80% or higher of customers getting their contact resolved on the first call to the call center (FCR) for three consecutive months or more.)

Jackson® is the marketing name for Jackson Financial Inc., Jackson National Life Insurance Company® (Home Office: Lansing, Michigan) and Jackson National Life Insurance Company of New York® (Home Office: Purchase, New York).

SAFE HARBOR STATEMENT

The information in this press release contains forward-looking statements about future events and circumstances and their effects upon revenues, expenses and business opportunities. Generally speaking, any statement in this release not based upon historical fact is a forward-looking statement. Forward-looking statements can also be identified by the use of forward-looking or conditional words, such as “could,” “should,” “can,” “continue,” “estimate,” “forecast,” “intend,” “look,” “may,” “expect,” “believe,” “anticipate,” “plan,” “predict,” “remain,” “future,” “confident” and “commit” or similar expressions. In particular, statements regarding plans, strategies, prospects, targets and expectations regarding the business and industry are forward-looking statements. They reflect expectations, are not guarantees of performance and speak only as of the dates the statements are made. We caution investors that these forward-looking statements are subject to known and unknown risks and uncertainties that may cause actual results to differ materially from those projected, expressed, or implied. Other factors that could cause actual results to differ materially from those in the forward-looking statements include those reflected in Part I, Item 1A. Risk Factors and Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations in our Annual Report on Form 10-K for the year ended December 31, 2025, as filed with the U.S. Securities and Exchange Commission (the “SEC”) on February 24, 2026, and elsewhere in the Company’s reports filed with the SEC. Except as required by law, Jackson Financial Inc. does not undertake to update such forward-looking statements. You should not rely unduly on forward-looking statements.

GENERAL DISCLOSURES

Jackson, its distributors, and their respective representatives do not provide tax, accounting, or legal advice. Any tax statements contained herein were not intended or written to be used and cannot be used for the purpose of avoiding U.S. federal, state, or local tax penalties. Tax laws are complicated and subject to change. Tax results may depend on each taxpayer’s individual set of facts and circumstances. You should rely on your own independent advisors as to any tax, accounting, or legal statements made herein.

Annuities are long-term, tax deferred vehicles designed for retirement and are insurance contracts. Variable annuities and registered index-linked annuities involve investment risks and may lose value. Earnings are taxable as ordinary income when distributed. Individuals may be subject to a 10% additional tax for withdrawals before age 59½ unless an exception to the tax is met.

Guarantees are backed by the claims-paying ability of Jackson National Life Insurance Company or Jackson National Life Insurance Company of New York. They are not backed by the broker/dealer from which this annuity contract is purchased, by the insurance agency from which this annuity contract is purchased or any affiliates of those entities, and none makes any representations or guarantees regarding the claims-paying ability of Jackson National Life Insurance Company or Jackson National Life Insurance Company of New York.

This material is authorized for use only when preceded or accompanied by the current contract prospectus. Before investing, investors should carefully consider the investment objectives and risks of the registered index-linked annuity. This and other important information is contained in the current contract prospectus at Jackson.com/ProspectusJMLP4NY for the Jackson Market Link Pro 4 (New York) prospectus, Jackson.com/ProspectusJMLP4 for the Jackson Market Link Pro 4 prospectus, Jackson.com/ProspectusJMLPA4NY for the Jackson Market Link Pro Advisory 4 (New York) prospectus or Jackson.com/ProspectusJMLPA4 for the Jackson Market Link Pro Advisory 4 prospectus.

The “S&P 500®” and the “Dow Jones Industrial Average®” (the “Indices”) are products of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”) and have been licensed for use by Jackson National Life Insurance Company (“Jackson”) and Jackson National Life Insurance Company of New York (“Jackson of NY”). S&P 500®, SPX®, SPY®, US 500, The 500, iBoxx®, iTraxx®, CDX®, The Dow®, DJIA®, and Dow Jones Industrial Average® are trademarks of S&P Global, Inc. or its affiliates (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Jackson and Jackson of NY. Jackson’s products are not sponsored or sold by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such products, nor do they have any liability for any errors, omissions, or interruptions of the indices.

The Jackson Market Link Pro Suite has been developed solely by Jackson National Life Insurance Company and Jackson National Life Insurance Company of New York. These products are not in any way connected to or sponsored, endorsed, sold or promoted by the London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). FTSE Russell is a trading name of certain of the LSE Group companies.

All rights in the Russell® 2000 (the “Index”) vest in the relevant LSE Group company which owns the index. Russell® is a trademark of relevant LSE Group company and is used by other LSE Group company under license.

The index is calculated by or on behalf of FTSE International Limited or its affiliate, agent or partner. The LSE Group does not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in the index or (b) investment in or operation of the Jackson Market Link Pro Suite. The LSE Group makes no claim, prediction, warranty or representation as to the results to be obtained from the Jackson Market Link Pro Suite or the suitability of the Index for the purpose to which it is being put by Jackson National Life Insurance Company and Jackson National Life Insurance Company of New York.

The Product referred to herein is not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such Products or any index on which such Products are based. The Contract contains a more detailed description of the limited relationship MSCI has with Jackson National Life Insurance Company and Jackson National Life Insurance Company of New York and any related Products.

Nasdaq®, Nasdaq-100®, Nasdaq-100 Index®, and NDX® are registered trademarks of Nasdaq, Inc. (which with its affiliates is referred to as the “Corporations”) and are licensed for use by Jackson National Life Insurance Company® (“Jackson”) and Jackson National Life Insurance Company of New York (“Jackson of NY”). The Product(s) have not been passed on by the Corporations as to their legality or suitability. The Product(s) are not issued, endorsed, sold, or promoted by the Corporations. THE CORPORATIONS MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO THE PRODUCT(S).

Registered index-linked annuities (contract form numbers ICC25 RILA310, ICC25 RILA310-CB1, ICC25 RILA312, ICC25 RILA312-CB1, ICC25 RILA315, ICC25 RILA315-FB1, ICC25 RILA317, ICC25 RILA317-FB1) are issued by Jackson National Life Insurance Company (Home Office: Lansing, Michigan) and in New York (contract form numbers RILA310NY, RILA310NY-CB1, RILA312NY, RILA312NY-CB1, RILA315NY, RILA315NY-FB1, RILA317NY, RILA317NY-FB1) by Jackson National Life Insurance Company of New York (Home Office: Purchase, New York) and distributed by Jackson National Life Distributors LLC, member FINRA. May not be available in all states and state variations may apply. These products have limitations and restrictions, including withdrawal charges or market value adjustments. Market value adjustments are not applied in New York. Jackson issues other annuities with similar features, benefits, limitations and charges. Discuss them with your financial professional or contact Jackson for more information.

VARIABLE ANNUITY DISCLOSURES

This material is authorized for use only when preceded or accompanied by the current contract prospectus and underlying fund prospectuses. Before investing, investors should carefully consider the investment objectives, risks, charges, and expenses of the variable annuity and its underlying investment options. This and other important information are contained in the current contract prospectus and underlying fund prospectuses. Please read the prospectuses carefully before investing or sending money.

On the contract anniversary on or immediately following the designated life’s attained age 59½, the for-life guarantee becomes effective provided: 1) the contract value is greater than zero and 2) the contract has not been annuitized. If the designated life is age 59½ on the effective date of the endorsement, then the for-life guarantee becomes effective on that date.

The latest income date allowed on variable annuity contracts is age 95, which is the required age to annuitize or take a lump sum.

Add-on benefits are available for an extra charge in addition to the ongoing fees and expenses of the variable annuity.

Variable annuities (contract form numbers VA775, VA775-CB1, VA775-RLC, ICC18 VA775, ICC18 VA775-CB1, ICC18 VA775-RLC, VA710, VA710-CB1, ICC19 VA710, ICC19 VA710-CB1, VA720, VA720-CB1, ICC19 VA720, ICC19 VA720-CB1, VA790, VA790-FB1, ICC17 VA790, ICC17 VA790-FB1, VA670, VA670-CB1, ICC19 VA670, ICC19 VA670-CB1, VA680, VA680-CB1, ICC19 VA680, ICC19 VA680-CB1, VA785, VA785-FB1, ICC18 VA785, ICC18 VA785-FB1) are issued by Jackson National Life Insurance Company (Home Office: Lansing, Michigan) and in New York (contract form numbers VA775NY, VA775NY-CB1, VA790NY, VA790NY-FB1, VA670NY, VA670NY-CB1, VA785NY, VA785NY-FB1) by Jackson National Life Insurance Company of New York (Home Office: Purchase, New York). Variable products are distributed by Jackson National Life Distributors LLC, member FINRA. These contracts have limitations and restrictions. Jackson issues other annuities with similar features, benefits, limitations, and charges. Discuss them with your financial professional or contact Jackson for more information.

Products and features may be limited by state availability, and/or your selling firm’s policies and regulatory requirements (including standard of conduct rules).

__________________________________

1 Jackson National Life Insurance Company is a wholly owned subsidiary of Jackson Financial Inc. Jackson Financial Inc. is a publicly traded company.

2 Investors are not buying shares of any stock or index and cannot invest directly in an index. The payment of dividends is not reflected in the index return.

3 Once the index account option value is removed from an index account option with a guaranteed cap crediting method, it cannot be reallocated into a new or existing guaranteed cap crediting method.

4 A performance lock ends the index account option term for the index account option out of which it is transferred, effectively terminating that index account option. Once a performance lock has been processed it is irrevocable. Therefore, when a performance lock is processed, the owner will not participate in additional gains or losses their chosen index may experience.

5 The rate enhancement option can not be elected when +Income is elected. +Income and the Rate Enhancement Option are not available in New York.

6 Owners could see a substantial loss during an index period if the index declines more than the level of downside protection. If an owner does see a substantial loss during an index period, the owner may not be able to participate fully in a subsequent market recovery due to the capped upside potential in subsequent index periods.

7 Not all crediting methods and/or protection options are available with all Index Account Option terms.

8 Performance Boost is a 10% boost that is credited if the index return is flat, positive, or negative within the buffer up to the stated performance boost cap rate.

9 State variations may apply. Owners will be eligible for this waiver of withdrawal charge after the first contract anniversary. If the owner or joint owner is confined to a nursing home or hospital for 90 consecutive days by medical necessity beginning after the contract issue date, you may access up to 100% of the contract value free of withdrawal charges. All contract values will be reduced proportionately. Taxes may apply.

10 State variations may apply. Owners will be eligible for this waiver of withdrawal charge after the first contract anniversary. If the owner or joint owner is diagnosed with a terminal illness that is expected to result in death within 12 months, you may access up to 100% of the contract value free of withdrawal charges. All contract values will be reduced proportionately. Taxes may apply.

11 If the oldest owner’s age when the contract is issued is between 0 and 80, the death benefit is equal to the greater of the current contract value or premiums paid into the contract adjusted for any withdrawals incurred since the issuance of the contract. If the oldest owner’s age is between 81 and 85 when the contract is issued, the death benefit is equal to the current contract value.

12 Withdrawals during the first six premium years are subject to a withdrawal charge or market value adjustment. Withdrawals before the end of a term are subject to an interim value adjustment which may have a positive or negative impact on the contract value at the end of the term and may be significant. Market value adjustments are not applied in New York.

NEW YORK–(BUSINESS WIRE)–

KBRA releases research on the National Association of Insurance Commissioners (NAIC) private letter ratings (PLR) review process. In August 2024, the NAIC passed an amendment that granted the Securities Valuation Office (SVO) the ability to review and challenge credit ratings that it does not believe are a reasonable measure of risk for regulatory purposes (the Discretion Amendment). Although the Discretion Amendment’s original January 2026 implementation has been delayed, it has focused attention on PLRs, the regulatory treatment of rated private assets, and the potential implications for U.S. life insurers’ risk-based capital (RBC) positions. KBRA views the potential impact of the Discretion Amendment through a measured analytical lens that considers the likely scope of reviews, the security-specific nature of potential outcomes, the distinction between required capital and statutory capital impairment, and the broader capital management tools available to insurers.

Key Takeaways

PLRs are not synonymous with private credit. While private credit represents an important part of the PLR market, PLRs may be associated with a range of asset types and transaction structures. The potential regulatory capital impact of a PLR review therefore depends on the specific security, its structure, collateral, rating level, and resulting NAIC designation.

Potential capital effects are likely to be security specific. KBRA expects the PLR review process to focus on individual securities or groups of securities with identified analytical or regulatory concerns. As a result, any RBC impact would likely depend on the size, rating category, NAIC designation, and insurer-level concentration of the affected holdings.

RBC sensitivity should be distinguished from economic loss. A change in statutory bond risk charges may increase authorized control level RBC (ACL), thereby lowering an RBC ratio if total adjusted capital (TAC) is unchanged. That outcome is different from a realized credit loss, impairment, or reduction in statutory surplus.

Company-level analysis should incorporate more than statutory RBC metrics. Insurer financial strength also depends on, among other things, asset-liability management, investment governance, earnings capacity, reinsurance arrangements, enterprise capital resources, and potential management actions.

For all credit ratings, whether published or unpublished, KBRA applies the same analytical approach, methodologies, rating scales, and controls through uniform rating committee processes and surveillance practices (see Unpublished Ratings: Same Standards, Different Distribution). The only distinction is in how the rating and associated reports are disseminated: For public ratings, this is accomplished through the KBRA website, while private ratings are distributed to the engaging entity through a virtual data room. KBRA publishes an annual Global Rating Stability and Transition Study, incorporating both published and private credit ratings, which indicates stability across the ratings universe. Other KBRA research has highlighted consistent performance for published and unpublished ratings (see Private Credit SF: How KBRA Ratings Stack Up).

KBRA, one of the major credit rating agencies, is registered in the U.S., EU, and the UK. KBRA is recognized as a Qualified Rating Agency in Taiwan, and is also a Designated Rating Organization for structured finance ratings in Canada. As a full-service credit rating agency, investors can use KBRA ratings for regulatory capital purposes in multiple jurisdictions.

NASHVILLE — The Tennessee Department of Commerce & Insurance (TDCI) proudly announces that over $107 million in insurance policies and benefits was located in 2025 for Tennesseans through the Life Insurance Policy Locator Service.

Developed by the National Association of Insurance Commissioners (NAIC), the Life Insurance Policy Locator Service is a free service that enables beneficiaries, executors, or legal representatives of deceased people to locatelife insurance policies and annuity contracts of their late family members, clients, or friends.

From Jan. 1, 2025, to Dec. 31, 2025, the service located insurance policies with $107,757,080 in benefits for Tennesseans, breaking the previous record of $87.67 million set in 2024.

“I am encouraged to see that Tennesseans are claiming life insurance benefits as these policies are intended by their purchasers to help cover financial burdens such as medical bills, funeral costs, and other financial obligations that can occur after the loss of a loved one,” said TDCI Commissioner Carter Lawrence. “It is my hope that the Life Insurance Policy Locator Service eases the burden that family members and loved ones may face after the passing of a loved one, and I am grateful that the NAIC created this program.”

Looking for a deceased loved one’s lost policy? TDCI recommends that you start by reviewing financial records to see if you can find where payments have been made to an insurance company. If any of the documents reference payments made to an insurance company, you can call them directly to see if a policy can be located.

To request a search, follow these steps:

Complete NAIC’s online Life Insurance Policy Locator Service request form. Once the request is complete, NAIC will send the policyholder’s information to all licensed life insurance companies across the United States.Companies will check their records to determine if they have a policy matching the beneficiary’s information.If a match is found, the company will respond within 60 days. If a company finds a match, they will respond directly to the requestor if you are a designated beneficiary or are legally authorized to receive such information.

The service does not track beneficiary information or claim payment after matches are reported, so there is no way to determine the amount actually returned to consumers. The total claim amount only includes the amount reported by companies tied to a match for a deceased person.

For more information on the Life Insurance Policy Locator Service and other consumer insurance resources, visit our blog or contact the TDCI Consumer Insurance Service Division at 1-800-342-4029 or (615) 741-2218.

, The 500

, The 500