Convertible market dynamics and the portfolio implications for insurers

By David A. Tyson and Andrew Willard

The convertible market has grown significantly in recent years, reflecting increased equity issuance and evolving corporate financing needs. As hybrid securities combining bond and equity characteristics, convertibles have historically delivered risk and return characteristics between equities and fixed income.

For insurers, convertibles may offer a way to enhance return potential while maintaining downside protection through the bond component. Credit quality, equity sensitivity and market composition remain key considerations for portfolio construction. As issuance expands and market conditions evolve, convertibles may play an increasing role in diversified insurance portfolios.

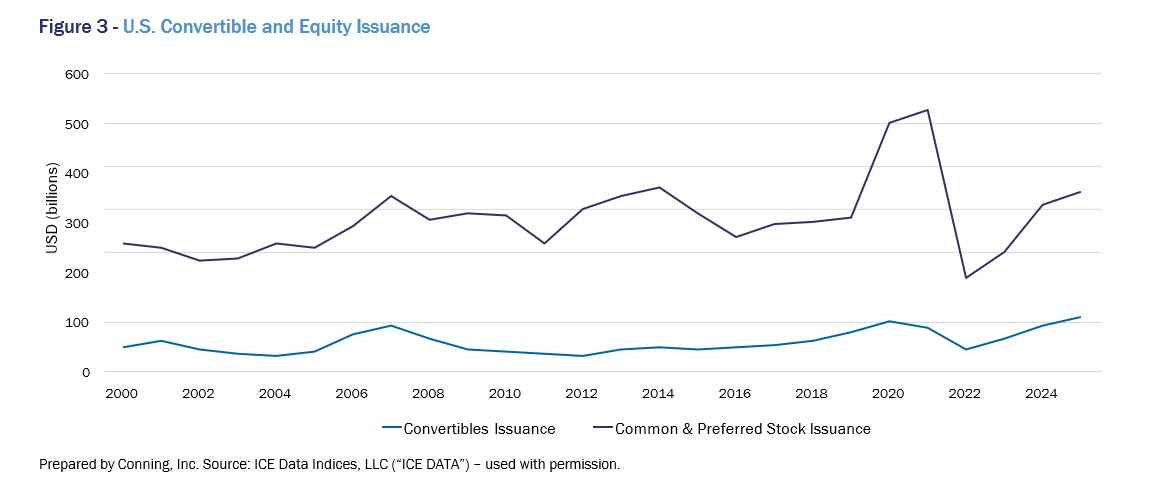

The convertible market has experienced a notable shift in issuance trends in recent years. Following a period of subdued issuance after the global financial crisis, activity increased significantly beginning in 2020. Issuance accelerated in 2020 and 2021 and has remained elevated, with 2024 and 2025 representing particularly strong years.

Structural characteristics of convertibles

Convertible securities combine features of both bonds and equities. The majority are structured as bonds, with a smaller portion issued as preferred stock.

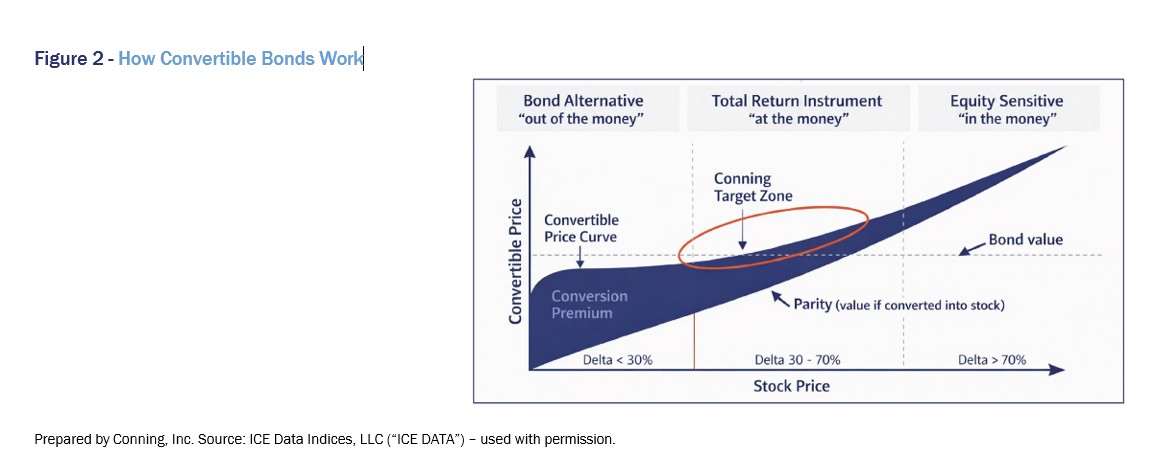

A key characteristic of convertibles is the presence of a bond value, which provides a floor supported by maturity and coupon payments. Over time, the relative importance of coupon income has declined, with bond floor protection increasingly driven by maturity value.

In addition to bond features, convertibles include an embedded option that allows participation in equity upside. As the underlying stock price increases, the value of the convertible rises accordingly.

However, as convertibles move further into equity-sensitive territory, their value converges toward equity value. Companies often call convertibles to encourage conversion into equity, particularly when the underlying stock performs well.

As equity prices decline, the bond component becomes more prominent, though increasing credit risk must be considered. This dynamic highlights the importance of credit analysis, particularly in lower price scenarios.

Issuance trends and market drivers

Convertible issuance has historically been closely correlated with equity issuance, with increases in equity issuance typically accompanied by higher convertible issuance.

Periods such as 2007 illustrate this relationship, when both equity and convertible issuance increased. At that time, a significant portion of issuance came from the financial sector, contributing to elevated exposure within convertible indices before the market dislocation in 2008.

Following the global financial crisis, both equity issuance and the number of publicly listed companies declined, contributing to a decline in convertible issuance throughout much of the 2010s.

In contrast, corporate bond issuance has continued to grow over time. However, when evaluated relative to overall equity market value, the market value of outstanding debt has not increased as a percentage of equity market value. This dynamic reflects the influence of rising equity market valuations, which have supported increased debt issuance capacity in capital markets.

Convertible issuance is not primarily driven by companies attempting to time the market. Rather, it is influenced by financing needs and the ability to access various sources of financing. As a result, issuance patterns reflect broader market conditions rather than tactical decision-making.

Convertibles as a financing tool

Convertibles function primarily as an equity-oriented financing instrument. Companies use them to raise capital for a variety of purposes, including funding growth initiatives, supporting balance sheets or maintaining credit ratings.

The events of 2020 illustrate this dynamic. During the pandemic, many companies faced increased financing needs. Convertible issuance increased significantly, reaching approximately $100 billion, as companies accessed both equity and convertible markets.

In some cases, convertibles were used alongside equity issuance to raise substantial capital. For example, companies seeking to preserve credit quality or maintain liquidity issued convertibles as part of broader capital-raising efforts.

Convertible issuance also reflects a company’s life cycle dynamic. Early-stage companies typically rely on bank financing before accessing public markets through an initial public stock offering. Following this transition, convertibles often represent an initial form of public market debt issuance, as traditional bond investors are less willing to invest in smaller or less diversified companies.

As a result, the convertible market includes a significant proportion of smaller or unrated issuers, reflecting its role in bridging equity and debt financing.

Convertible segments and return sensitivity

Convertibles can be broadly categorized based on their sensitivity to the underlying equity:

• Out-of-the-money (bond alternatives):

Securities where the stock price is well below the conversion price, behaving more like bonds.

• At-the-money (balanced exposure):

Securities where bond and equity values are closely aligned. These typically exhibit moderate equity sensitivity and are often the focus of portfolio allocation.

• In-the-money (equity-sensitive):

Securities with significant equity exposure, often trading at higher prices and demonstrating stronger sensitivity to stock movements.

Most new issues are in the “at-the-money” segment, which typically offers the highest balance between bond protection and equity participation (and is often the primary focus for our portfolio construction.) As the underlying stock moves over time, the convertibles then move into the in-the-money category if the stock does well or if the stock falls, the convertible falls into the out-of-the money category. Ongoing portfolio management keeps the overall portfolio’s risk profile in line with objectives.

Market composition and credit considerations

The convertible market includes a large proportion of unrated securities, with typically 75-80% of the universe falling into this category. This reflects the presence of smaller or earlier-stage companies.

Despite this composition, higher-quality opportunities exist within the market, including many issuers that exhibit characteristics consistent with investment-grade or near-investment-grade profiles.

Portfolio construction for insurers often emphasizes higher-quality issuers to preserve downside protection through the bond component of convertibles. Credit analysis remains a critical component in evaluating risk, particularly when equity prices decline and credit exposure becomes more important.

Return characteristics and benchmark behavior

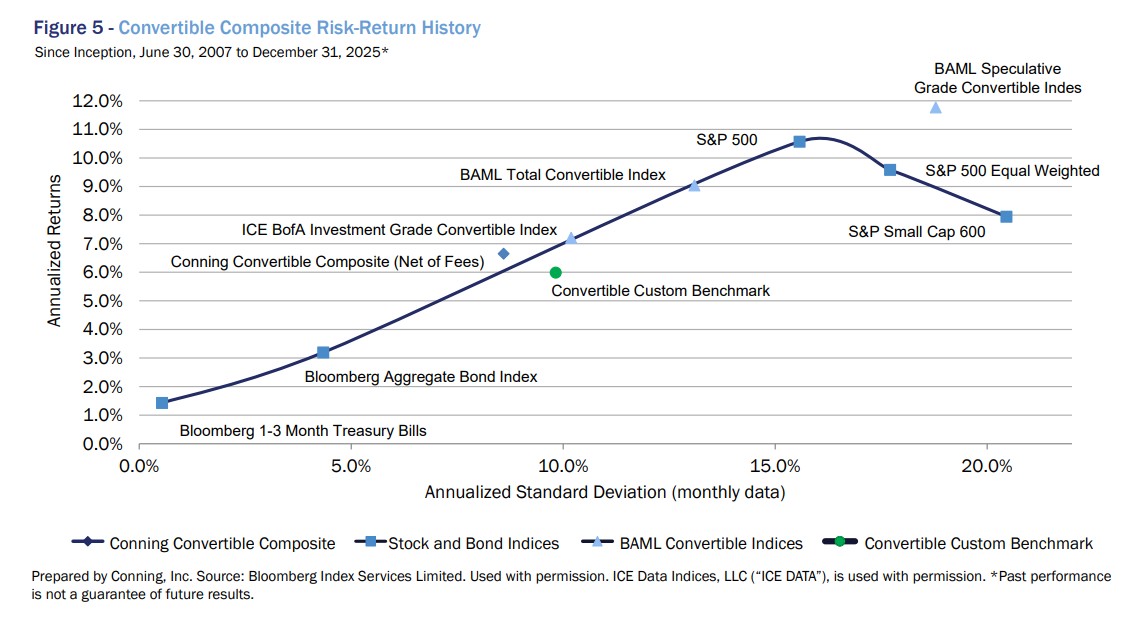

Convertible returns have historically been positioned between equity and fixed income markets. Performance observations indicate that returns have been generated between the S&P 500 and the Bloomberg Aggregate Bond Index.

While shorter-term performance may deviate, particularly during periods when equity market performance is dominated by a small number of companies, longer-term outcomes have aligned with the objective of delivering risk and return characteristics between stocks and bonds.

Different segments of the convertible market exhibit varying levels of risk. Speculative-grade convertibles tend to demonstrate higher volatility, while investment-grade convertibles typically align more closely with a balanced risk profile between equities and bonds.

Portfolio positioning and strategy considerations

Portfolio construction within convertibles involves balancing credit quality and equity sensitivity. Emphasis is often placed on maintaining exposure within the intermediate “at-the-money” range, where the trade-off between risk and return is most balanced.

Portfolio and benchmark allocations shift as market conditions evolve, with issuance patterns and equity performance influencing portfolio exposures.

Differences between portfolio positioning and benchmark composition can result in tracking variation, reflecting the range of approaches available in managing convertible portfolios.

Why this matters for insurers

For insurers, convertible securities offer a way to balance return objectives with downside protection. In environments where equity valuations are elevated or fixed income returns are constrained, convertibles can provide partial equity participation while maintaining the defensive characteristics of bonds. Portfolio allocations can focus on higher-quality issuers and at-the-money securities to balance credit risk and equity sensitivity. Convertibles serve as a complementary allocation within surplus or total return portfolios, particularly for insurers seeking diversification and intermediate risk exposure between equities and traditional fixed income.

Convertible issuance has increased significantly in recent years, reflecting stronger equity market conditions and corporate financing needs. As a hybrid instrument, convertibles continue to serve as a bridge between equity and debt markets, with issuance patterns closely aligned with equity activity.

The structural characteristics of convertibles support return outcomes between equities and fixed income, consistent with their role in portfolio construction.

For insurers, convertibles offer a flexible asset class that can be positioned to balance downside protection and equity participation, with outcomes dependent on credit quality, market conditions, and portfolio allocation decisions.

As insurers continue to evaluate portfolio resilience, return generation, and diversification, convertibles may represent a useful tool within a broader portfolio strategy. Their hybrid characteristics allow insurers to participate in equity upside while maintaining elements of downside protection, making them particularly relevant in environments where balancing risk and return remains a key objective.

David A. Tyson, Ph.D., CFA, is a managing director and portfolio manager at Conning. Contact him at david.tyson@innfeedback.com.

Andrew Willard is an assistant vice president for equity strategies on Conning’s portfolio management team. Contact him at andrew.willard@innfeedback.com.

© Entire contents copyright 2026 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

The post Convertible market dynamics and the portfolio implications for insurers appeared first on Insurance News | InsuranceNewsNet.