MONTPELIER, Vt.–(BUSINESS WIRE)– National Life Group recently named Jason Doiron Chief Executive Officer of its investment affiliate, NLG Capital, as the organization continues to focus on strategic growth. Doiron is also Executive Vice President and Chief Investment Officer of National Life Group.

Jason Doiron, Chief Executive Officer of NLG Capital

As CEO of NLG Capital, Doiron will be responsible for supporting the ongoing growth of the overall organization. As CIO, he sets the investment strategy and asset allocations for National Life Group’s investment portfolios.

“Jason is an innovative leader whose deep investment expertise has helped position National Life Group among the top 10 life insurance companies*,” said Chair, CEO, and President Mehran Assadi. “His commitment to the business and proven track record of accelerating growth in volatile markets are exceptional. He is well positioned to succeed as CEO of NLG Capital.”

Doiron was named Chief Investment Officer of National Life Group in 2016. As CIO, he led the build-out of NLG Capital into an industry-leading proprietary asset management platform, overseeing the expansion of the investment team and the opening of the firm’s New York City office. During his tenure as CIO, National Life Group’s assets have grown from less than $20 billion in 2016 to more than $65 billion today, with NLG Capital serving as a key driver of the organization’s competitive edge.

Doiron joined National Life Group in 2008 as Head of Derivatives and was named Portfolio Manager of the General Account and Head of Fixed Income in 2010. He subsequently took on portfolio management responsibilities across several Sentinel mutual funds before being appointed Head of Investments for Sentinel — National Life Group’s wholly owned asset management subsidiary — in 2013, a role he held through Sentinel’s sale in 2018.

Earlier in his career, Doiron was Director of Quantitative Trading – U.S. Debt Markets for the Royal Bank of Canada’s Capital Markets group, and prior to that held a position with Citigroup Global Investments.

Doiron earned an MBA from the University of Chicago Graduate School of Business and a BA from the University of Maine at Farmington. He holds both the Financial Risk Manager (FRM) and Professional Risk Manager (PRM) designations.

About National Life Group

National Life Group has been keeping promises since 1848, providing access to flexible, secure life insurance and annuities for families, businesses, educators, and first responders nationwide. With an independent, entrepreneurial spirit, our values are to “Do good, Be good, Make good” for our customers, agents, employees, and the communities we serve. Learn more at NationalLife.com.

National Life Group® is a trade name of National Life Insurance Company (NLIC), Montpelier, VT founded in 1848, Life Insurance Company of the Southwest (LSW), Addison, TX chartered in 1955, and its affiliates. Each company is solely responsible for its own financial condition and contractual obligations. LSW is not an authorized insurer in New York and does not conduct insurance business in New York. NLIC, the flagship of National Life Group was founded in 1848, and all references to 1848 are attributable to NLIC.

Products are issued by National Life Insurance Company and Life Insurance Company of the Southwest.

NLG Capital is the registered investment advisor affiliate of National Life Group responsible for managing the organization’s investment portfolios.

Life and annuity carrier executives are concerned about a critical issue – the increasing cost of customer acquisition, driven in part by the commission structure of products sold through third-party distribution. A heavy reliance on TPD is unavoidable – career agency/captive agent models have continued to lose overall market share. And the DTC channel has not reached a level of maturity to achieve a significant premium for most carriers.

Chris Taylor

But carriers also need to solve for cost – significant commission costs put pressure on the carrier to maintain lower lapse rates for long-term profitability. But without truly “owning” the customer relationship, persistency can be difficult.

Carriers have historically managed persistency in five ways:

Persistency-based incentive compensation

Predictive analytics and data-driven (e.g., lapse models)

Product design and features

Automated payment facilitation and communications

Underwriting and suitability standards

But managing lapses addresses the long-term profitability of the customer, not the cost of acquiring the customer.

To address the cost, carriers need a new strategy – a DTC/advisor hybrid channel.

Reimagining the purchase journey

The DTC channel has historically struggled as a serious channel for a variety of reasons – product complexity, lack of advisor touch, poor sales tools, etc. This has caused many carriers to retreat from the DTC channel.

But consumer behavior has shifted decisively toward digital. According to the 2025 LIMRA/Life Happens Insurance Barometer Study, 92% of consumers now research life insurance online (up from 71% a decade ago), yet only 25% are ready to complete the entire purchase DTC. The remaining 75% explicitly want professional guidance at key decision points. This creates the perfect conditions for a customer-opt-in hybrid model that maximizes low-cost digital volume while delivering high-intent leads to advisors.

Two key insights for carriers:

Some customers are ready for a purely digital insurance purchase experience.

A digital-first sales process can provide a strong lead program for advisors.

For carriers, this means designing a process that begins with education and strong digital sales tools across all products. Carriers should design this purchase experience to allow a customer to opt into a direct purchase. That is the best-case scenario for a carrier – no commission paid and an accelerated path to profitability.

More important is the customer’s ability to off-ramp from the digital-first experience and move to a financial advisor at any point. A key decision for carriers is what level of purchase experience the carrier wants to provide – this could range from a full purchase experience across all products to developing only a qualified lead program.

Addressing carrier concerns

One common carrier concern is lead leakage: What happens if an advisor receives the warm lead and ultimately places the business with a competing carrier? Industry data shows this risk is already baked into third-party distribution — advisors typically place only 49%-54% of life insurance with their primary carrier. The DTC/agent hybrid improves the carrier’s position: it can dramatically lower overall acquisition cost (replacing 80% or more of first-year commissions with modest lead fees or shared compensation). Carriers that feed advisors high-quality, context-rich leads consistently report stronger long-term partner relationships and improved wallet share over time.

What it takes for carriers to win

For L/A carriers interested in developing this program, execution remains everything, but there are clear requirements for success:

World-class end-to-end DTC platform — Intuitive user experience, simplified product variants for self-serve, AI-assisted underwriting and real-time issuance capabilities

Intelligent, non-intrusive opt-in prompts — Triggered by user behavior (e.g., time on complex pages, repeated questions or quote review) with clear value propositions

Seamless, context-rich advisor handoff — Prepopulated applications, shared digital session and advisor dashboards so the warm lead feels effortless.

Balanced compensation and incentives — Tiered structures that reward DTC volume for the carrier while giving agents attractive economics on opted-in leads

Robust analytics and testing — Predictive models to flag when a prospect might benefit from advisor help

Strong compliance and suitability framework — Clear consent flows, audit trails and product guardrails to avoid mis-selling risks on either path

Targeted marketing + pilot approach — Focus on segments most likely to self-serve or benefit from choice; start with simpler products before expanding to full life/annuity suites.

Distribution partner alignment — Transparent communication that this platform augments their business with higher-quality, lower-effort leads.

Carriers that nail the digital foundation and behavioral nudges can achieve lower acquisition costs, higher customer satisfaction and a scalable model that works for both self-directed buyers and those who value advice. This doesn’t replace persistency/lapse management. Indeed, the combination of reduced acquisition costs and a focus on persistency improves the entire economics.

This is a significant investment, but shifting digital expectations, particularly for younger generations, will force carriers to embrace this new age.

Since the 2020 pandemic, life insurance sales have surged. In 2025, policy counts jumped 7% year over year, but there remains work to be done, LIMRA researchers say.

“Despite these record sales, we haven’t seen a meaningful decline in the life insurance needs gap,” Bryan Hodgens, head of LIMRA research, said during a recent LinkedIn Live titled, “Understanding the Elusive Life Insurance Consumer.”

Hodgens was joined by Steve Wood, research director for LIMRA’s Markets Research, to discuss results from the 2026 Insurance Barometer Study, conducted jointly by nonprofit industry trade associations LIMRA and Life Happens.

“When the pandemic hit in 2020, we saw a fairly significant rise in the people who said they don’t have life insurance and need to buy some or they have some and need more,” Wood said.

Wood said the pandemic led to a rise in awareness of the need for life insurance, as there was a lot of premature mortality. Despite better health outcomes and vaccines, that awareness stayed elevated for five or six years, but it started dropping last year.

Since LIMRA, along with some of its member companies, has been in business for over 100 years, researchers were able to look back to 1918 and compare the rise in interest in life insurance following the influenza pandemic in that year.

“It matches almost perfectly what we saw from the 2020 pandemic. It’s about a four-year tail in interest in life insurance following a global pandemic,” Wood said.

During the LinkedIn Live, they discussed the many factors impacting life insurance sales, including demographics, technology advances, changes in distribution and overestimating the cost.

“By 2030, there will be more people over 65 than under 30,” Hodgens said, noting that the advisor population is also aging.

At the same time, Wood notes that younger generations are delaying or rejecting entirely life events like marriage or starting a family. “We know that’s a huge driver in first-time life insurance purchasing,” Wood said.

‘Personal connections’ are key

Additionally, the industry is using artificial intelligence and other new technologies to streamline the digital process, underwriting, and the speed to market.

“All of these technological advancements are helping more people understand life insurance in a simpler, faster way,” Wood said. “That is allowing our human agents to make those personal connections, which ultimately is what drives sales of more life insurance.”

This is important because the 2026 Insurance Barometer study revealed that 40% of Americans have little or no understanding of life insurance.

“People don’t buy what they don’t understand,” Wood noted. “So how do we get them to understand what life insurance is, how it works and how it’s really different from health insurance or property and casualty insurance?”

Another potential barrier to some people getting life insurance may be a misunderstanding of the cost of life insurance.

In the most-recent Barometer study, instead of just asking them about one particular policy, the study asked respondents about themselves and how much a very basic $250,000 level term, 20-year policy would be for them.

They were asked to rate their health on a scale of one to 10, and then LIMRA developed a matrix pricing for that person.

“What we find probably isn’t surprising, but essentially the younger and healthier a person is, the more they overestimate – often by as much as 10 times the actual cost – what that policy would be for them,” Wood said.

Wood said that younger people think life insurance is as much as $1,200 a year when, in fact, the younger and healthy you are, the cheaper it is to buy life insurance.

Entire contents copyright 2026 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Ann Moran Heiss, age 96, of Danvers and formerly of Dalton and Pittsfield, Massachusetts, passed away peacefully on April 27, 2026. Ann was born on Long Island, New York, the beloved daughter of Edward and Martha Moran, and the cherished sister of her late brothers, Edward and John.

The sudden passing of her father at age 42 required Ann to enter the workforce immediately after graduating from Lynbrook High School, rather than pursuing her plans for college. In 1952, while working as a secretary in New York City, she was introduced to her future husband, Everett Heiss, of Queens Village, New York. They were married in 1954, lived briefly in Detroit, Michigan, and then settled in the Berkshires when Everett began his career with Berkshire Life Insurance Company in Pittsfield. They raised their three children in nearby Dalton and later moved to Pittsfield.

Ann was a devoted mother, a Camp Fire Girls leader, and a communicant of St. Agnes Church in Dalton. Once her children were in school full-time, she began working as a teacher’s aide at Dalton Junior High School. Approaching the age of 40, she made the decision to pursue her long-held dream of higher education. She graduated 1930-2026

from Berkshire Community College and later North Adams State College with honors, earning her teaching degree. Ann went on to work in the Pittsfield and Cheshire school systems as a Reading Specialist. In later years, she also obtained her real estate license, assisting clients and friends throughout the Berkshires.

Ann was known for her great sense of humor and her generous, kind heart. She rooted for the underdog, was quick to laugh, and took joy in writing thoughtful notes to those she loved. She and Everett shared a love of music and dancing, especially as members of the Votre Soirée dance group, where they gathered monthly with close friends. They also enjoyed traveling throughout the US in their RV, exploring several national parks.

Ann’s compassion was evident in her actions—whether bringing gifts to a family displaced by a Christmas house fire, volunteering at a hospital gift shop, or helping Spanish-speaking workers adjust to new jobs by assisting with English. She was an active member of the philanthropic educational organization P.E.O., supporting women in their pursuit of education.

Ann and Everett built a life rich in friendship and community, both in the Berkshires and in Florida, where they spent 26 winters. Together, they celebrated more than 71 years of marriage.

Ann is survived by her devoted husband, Everett; her beloved children and their spouses: Barbara (Robert Goodwill), Susan McDermott (Robert), and Brian (Sydney); her grandchildren and their spouses, Sara McDermott (Jon McManus), Jeff McDermott (Kristen), Emily Heiss, and Anna Heiss; and her two great-grandchildren, Annie and Claire McDermott, as well as many nieces and nephews.

She will be deeply missed by all who knew and loved her.

FUNERAL NOTICE: A liturgy of Christian Burial will be held Tuesday May 5, 2026 at 11 am at St. Agnes Church, Main Street Dalton, celebrated by Rev. Brian Mc-Grath. Burial will follow in Pittsfield Cemetery. Receiving hour will be held at the church beginning at 10:15.

In lieu of flowers, memorial donations may be made in her name to: Care Dimensions of Danvers c/o Dery Funeral Home 54 Bradford St. Pittsfield MA 01201

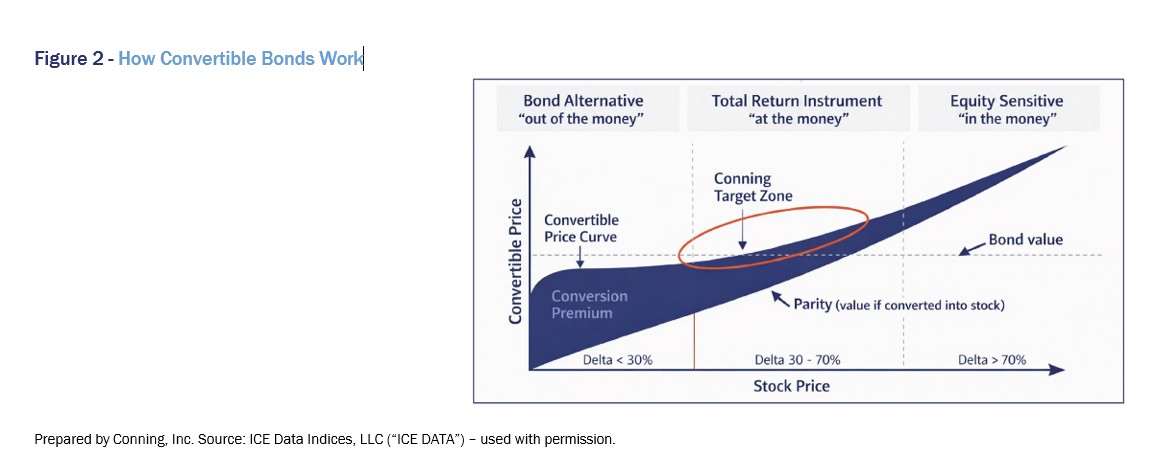

The convertible market has grown significantly in recent years, reflecting increased equity issuance and evolving corporate financing needs. As hybrid securities combining bond and equity characteristics, convertibles have historically delivered risk and return characteristics between equities and fixed income.

David A. Tyson

For insurers, convertibles may offer a way to enhance return potential while maintaining downside protection through the bond component. Credit quality, equity sensitivity and market composition remain key considerations for portfolio construction. As issuance expands and market conditions evolve, convertibles may play an increasing role in diversified insurance portfolios.

Andrew Willard

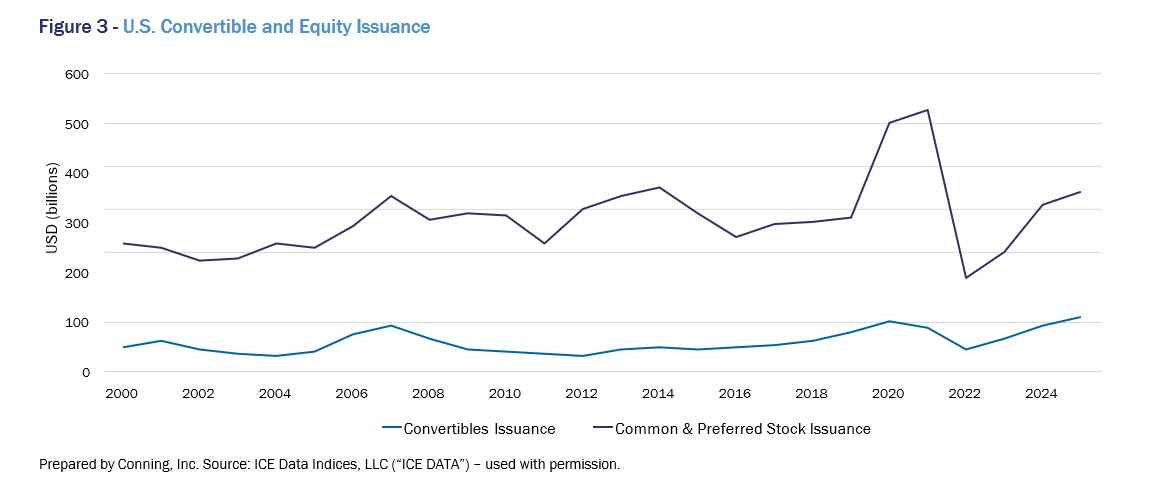

The convertible market has experienced a notable shift in issuance trends in recent years. Following a period of subdued issuance after the global financial crisis, activity increased significantly beginning in 2020. Issuance accelerated in 2020 and 2021 and has remained elevated, with 2024 and 2025 representing particularly strong years.

Structural characteristics of convertibles

Convertible securities combine features of both bonds and equities. The majority are structured as bonds, with a smaller portion issued as preferred stock.

A key characteristic of convertibles is the presence of a bond value, which provides a floor supported by maturity and coupon payments. Over time, the relative importance of coupon income has declined, with bond floor protection increasingly driven by maturity value.

In addition to bond features, convertibles include an embedded option that allows participation in equity upside. As the underlying stock price increases, the value of the convertible rises accordingly.

However, as convertibles move further into equity-sensitive territory, their value converges toward equity value. Companies often call convertibles to encourage conversion into equity, particularly when the underlying stock performs well.

As equity prices decline, the bond component becomes more prominent, though increasing credit risk must be considered. This dynamic highlights the importance of credit analysis, particularly in lower price scenarios.

Issuance trends and market drivers

Convertible issuance has historically been closely correlated with equity issuance, with increases in equity issuance typically accompanied by higher convertible issuance.

Periods such as 2007 illustrate this relationship, when both equity and convertible issuance increased. At that time, a significant portion of issuance came from the financial sector, contributing to elevated exposure within convertible indices before the market dislocation in 2008.

Following the global financial crisis, both equity issuance and the number of publicly listed companies declined, contributing to a decline in convertible issuance throughout much of the 2010s.

In contrast, corporate bond issuance has continued to grow over time. However, when evaluated relative to overall equity market value, the market value of outstanding debt has not increased as a percentage of equity market value. This dynamic reflects the influence of rising equity market valuations, which have supported increased debt issuance capacity in capital markets.

Convertible issuance is not primarily driven by companies attempting to time the market. Rather, it is influenced by financing needs and the ability to access various sources of financing. As a result, issuance patterns reflect broader market conditions rather than tactical decision-making.

Convertibles as a financing tool

Convertibles function primarily as an equity-oriented financing instrument. Companies use them to raise capital for a variety of purposes, including funding growth initiatives, supporting balance sheets or maintaining credit ratings.

The events of 2020 illustrate this dynamic. During the pandemic, many companies faced increased financing needs. Convertible issuance increased significantly, reaching approximately $100 billion, as companies accessed both equity and convertible markets.

In some cases, convertibles were used alongside equity issuance to raise substantial capital. For example, companies seeking to preserve credit quality or maintain liquidity issued convertibles as part of broader capital-raising efforts.

Convertible issuance also reflects a company’s life cycle dynamic. Early-stage companies typically rely on bank financing before accessing public markets through an initial public stock offering. Following this transition, convertibles often represent an initial form of public market debt issuance, as traditional bond investors are less willing to invest in smaller or less diversified companies.

As a result, the convertible market includes a significant proportion of smaller or unrated issuers, reflecting its role in bridging equity and debt financing.

Convertible segments and return sensitivity

Convertibles can be broadly categorized based on their sensitivity to the underlying equity:

• Out-of-the-money (bond alternatives):

Securities where the stock price is well below the conversion price, behaving more like bonds.

• At-the-money (balanced exposure):

Securities where bond and equity values are closely aligned. These typically exhibit moderate equity sensitivity and are often the focus of portfolio allocation.

• In-the-money (equity-sensitive):

Securities with significant equity exposure, often trading at higher prices and demonstrating stronger sensitivity to stock movements.

Most new issues are in the “at-the-money” segment, which typically offers the highest balance between bond protection and equity participation (and is often the primary focus for our portfolio construction.) As the underlying stock moves over time, the convertibles then move into the in-the-money category if the stock does well or if the stock falls, the convertible falls into the out-of-the money category. Ongoing portfolio management keeps the overall portfolio’s risk profile in line with objectives.

Market composition and credit considerations

The convertible market includes a large proportion of unrated securities, with typically 75-80% of the universe falling into this category. This reflects the presence of smaller or earlier-stage companies.

Despite this composition, higher-quality opportunities exist within the market, including many issuers that exhibit characteristics consistent with investment-grade or near-investment-grade profiles.

Portfolio construction for insurers often emphasizes higher-quality issuers to preserve downside protection through the bond component of convertibles. Credit analysis remains a critical component in evaluating risk, particularly when equity prices decline and credit exposure becomes more important.

Return characteristics and benchmark behavior

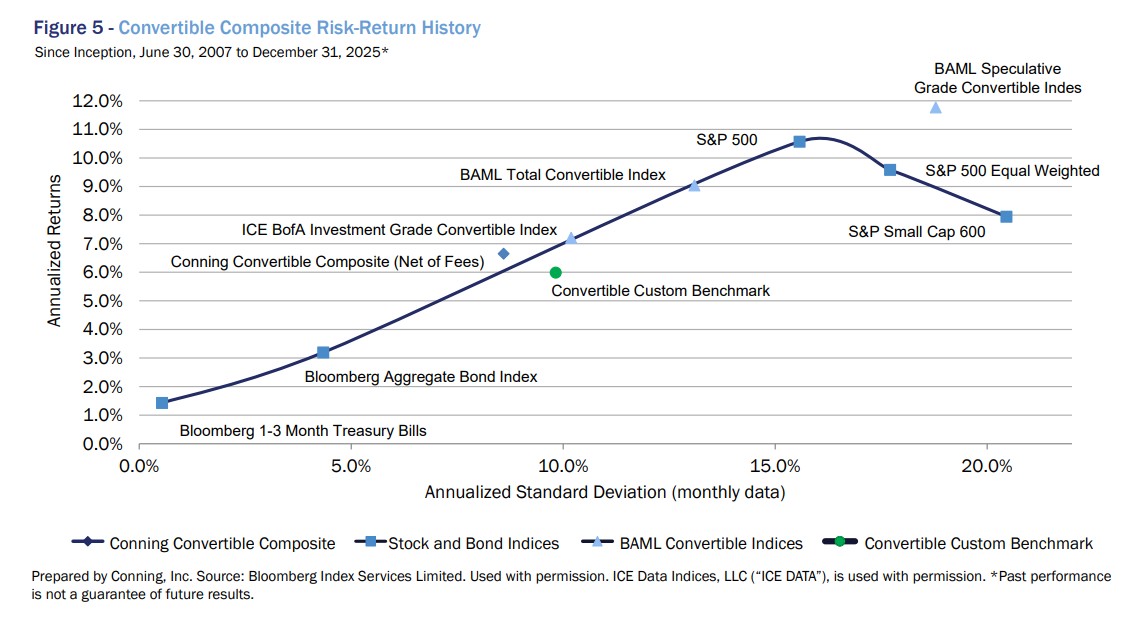

Convertible returns have historically been positioned between equity and fixed income markets. Performance observations indicate that returns have been generated between the S&P 500 and the Bloomberg Aggregate Bond Index.

While shorter-term performance may deviate, particularly during periods when equity market performance is dominated by a small number of companies, longer-term outcomes have aligned with the objective of delivering risk and return characteristics between stocks and bonds.

Different segments of the convertible market exhibit varying levels of risk. Speculative-grade convertibles tend to demonstrate higher volatility, while investment-grade convertibles typically align more closely with a balanced risk profile between equities and bonds.

Portfolio positioning and strategy considerations

Portfolio construction within convertibles involves balancing credit quality and equity sensitivity. Emphasis is often placed on maintaining exposure within the intermediate “at-the-money” range, where the trade-off between risk and return is most balanced.

Portfolio and benchmark allocations shift as market conditions evolve, with issuance patterns and equity performance influencing portfolio exposures.

Differences between portfolio positioning and benchmark composition can result in tracking variation, reflecting the range of approaches available in managing convertible portfolios.

Why this matters for insurers

For insurers, convertible securities offer a way to balance return objectives with downside protection. In environments where equity valuations are elevated or fixed income returns are constrained, convertibles can provide partial equity participation while maintaining the defensive characteristics of bonds. Portfolio allocations can focus on higher-quality issuers and at-the-money securities to balance credit risk and equity sensitivity. Convertibles serve as a complementary allocation within surplus or total return portfolios, particularly for insurers seeking diversification and intermediate risk exposure between equities and traditional fixed income.

Convertible issuance has increased significantly in recent years, reflecting stronger equity market conditions and corporate financing needs. As a hybrid instrument, convertibles continue to serve as a bridge between equity and debt markets, with issuance patterns closely aligned with equity activity.

The structural characteristics of convertibles support return outcomes between equities and fixed income, consistent with their role in portfolio construction.

For insurers, convertibles offer a flexible asset class that can be positioned to balance downside protection and equity participation, with outcomes dependent on credit quality, market conditions, and portfolio allocation decisions.

As insurers continue to evaluate portfolio resilience, return generation, and diversification, convertibles may represent a useful tool within a broader portfolio strategy. Their hybrid characteristics allow insurers to participate in equity upside while maintaining elements of downside protection, making them particularly relevant in environments where balancing risk and return remains a key objective.

David A. Tyson, Ph.D., CFA, is a managing director and portfolio manager at Conning. Contact him at david.tyson@innfeedback.com.

Andrew Willard is an assistant vice president for equity strategies on Conning’s portfolio management team. Contact him at andrew.willard@innfeedback.com.

FRANKFORT, Ky.–(BUSINESS WIRE)–

Investors Heritage Life Insurance Company (“Investors Heritage”) is pleased to announce that Anna Reynolds was promoted to Senior Vice President and General Counsel effective 2025.

Ms. Reynolds joined Investors Heritage in 2017 and has previously served as Associate General Counsel and Assistant Vice President. Since joining the company, she has provided strategic legal and regulatory guidance across all aspects of the business, supporting the company’s long-term growth and governance priorities while navigating an increasingly complex and evolving compliance environment.

Ms. Reynolds brings a depth of legal expertise, professionalism, and sound judgment to her executive leadership role. She works closely and collaboratively with departments across the organization and is widely regarded as a trusted, solutions-oriented partner who balances legal rigor with practical business insight.

“Anna has consistently demonstrated sharp legal insight, thoughtful leadership, and an unwavering commitment to our company and its values,” said Robert M. Hardy, Jr., Chief Executive Officer of Investors Heritage. “Her ability to work effectively across departments has earned her the respect and trust of colleagues throughout the organization, and I’m excited to see her continue to serve in this executive leadership role.”

Ms. Reynolds earned her Juris Doctor from Northeastern University School of Law and holds a Bachelor of Science degree from Purdue University. Her promotion reflects Investors Heritage’s long‑term commitment to disciplined leadership and building an organization positioned for sustainable growth over time.

Investors Heritage congratulates Ms. Reynolds on this well‑deserved promotion and looks forward to her continued contributions as a member of the company’s senior leadership team.

About Investors Heritage and Aquarian Holdings

Founded in 1960, Investors Heritage Life Insurance Company offers life insurance and annuity products that help individuals plan for retirement and preserve their legacies. Headquartered in Kentucky and licensed in nearly every U.S. state, Investors Heritage combines deep regional roots with a national presence—delivering forward-thinking, tech-enabled solutions grounded in the enduring value of personal service.

Investors Heritage is an insurance carrier within Aquarian Insurance Holdings, the insurance arm of Aquarian Holdings. Aquarian Holdings is a diversified global holding company with insurance and asset management solutions, supporting long-term growth through strategic capital and operational expertise.

Woods Aitken LLP, along with the Lincoln Human Resource Management Association and the Lincoln Journal Star, have announced the finalists for the 2026 Best Places to Work in Lincoln awards.

The awards are determined based on the results of the Best Places to Work in Lincoln survey conducted earlier this year.

Finalists are split into four categories based on workforce size, with three finalists each in the small, medium, large and extra-large categories.

Winners for each category will be announced at a June 4 celebration at Haymarket Park.

Here are this year’s finalists, listed in alphabetical order in each category:

Small companies (10-24 employees): Americom Communications, Custom Blinds & Design and Wellbeing Initiative, Inc.

Medium Companies (25-49 employees): Cerris Systems North Central, HoriSun Hospice and RentVision.

Large Companies (50-199 employees): JEO Consulting Group, NMPP Energy and Region 5 Systems.

Extra-Large Companies (200+ employees): Ameritas Life Insurance Corp., Assurity Life Insurance Company and Olsson.

OLDWICK, N.J.–(BUSINESS WIRE)– AM Best has affirmed the Financial Strength Rating (FSR) of A+ (Superior) and the Long-Term Issuer Credit Ratings (Long-Term ICRs) of “aa-” (Superior) of the members of Old Republic Insurance Companies (Old Republic). Concurrently, AM Best has affirmed the FSR of A+ (Superior) and the Long-Term ICRs of “aa-” (Superior) of Old Republic National Title Insurance Company (Tampa, FL) and American Guaranty Title Insurance Company (Oklahoma City, OK) (collectively referred to as Old Republic Title Insurance Group [ORTIG]). In addition, AM Best has affirmed the FSR of A- (Excellent) and the Long-Term ICR of “a-” (Excellent) of Old Republic Life Insurance Company (ORL) (Chicago, IL). At the same time, AM Best has affirmed the FSR of A (Excellent) and the Long-Term ICR of “a+” (Excellent) of Old Republic Insurance Company of Canada (Old Republic Canada) (Hamilton, Ontario). The outlook of these Credit Ratings (ratings) is stable.

All companies are subsidiaries of Old Republic International Corporation (ORI) [NYSE: ORI]. (See below for a detailed listing of the companies and ratings for the members of Old Republic.)

The ratings of Old Republic, which is considered the lead rating unit in the ORI enterprise, reflect its balance sheet strength, which AM Best assesses as strongest, as well as its strong operating performance, favorable business profile and appropriate enterprise risk management (ERM).

Old Republic is the flagship group for the Old Republic Insurance enterprise and one of the top 50 property/casualty insurers in the United States. The group is made up of commercial lines insurance carriers that provide underwriting and risk management services for business partners across the North America economy. The group’s largest lines of business include commercial auto and workers’ compensation; however, it continues to expand product capabilities beyond the traditional focus within these lines. Old Republic benefits from its expertise within the alternative risk transfer market and specialty commercial segments, as well as historically strong earnings, expertise in its respective individual business specialties and well-recognized franchises. The organization continues to have very modest exposure to asbestos liabilities.

The ratings of ORTIG reflect its balance sheet strength, which AM Best assesses as strongest, as well as its adequate operating performance, neutral business profile and appropriate ERM. The ratings of ORTIG also reflect the implicit support the group receives from its position in the Old Republic enterprise and its strategic role within the organization.

The ratings of ORTIG also recognize its strong reserving practices and continued profitability. With a majority of ORTIG’s premiums and fees generated through independent agents, a significant portion of its expenses are variable. This enables ORTIG to manage down cycles better, as fixed costs generally are lower for that distribution channel. AM Best expects that ORTIG will continue to generate underwriting and operating results that are in line with its title insurance competitors. AM Best expects that ORTIG will remain a significant contributor to the overall profitability of the ORI enterprise, while maintaining the strongest level of risk-adjusted capitalization in the intermediate term, as measured by Best’s Capital Adequacy Ratio (BCAR). ORTIG continues to be integral to the overall organization, with common branding and talent synergies, as well as complementary ERM programs.

The ratings of ORL reflect its balance sheet strength, which AM Best assesses as very strong, as well as its adequate operating performance, limited business profile and appropriate ERM.

The ratings of ORL also reflect its risk-adjusted capitalization, which is assessed at the strongest level, as measured by BCAR. Invested asset holdings are of good credit quality, as the portfolio is designed to minimize credit default risk rather than maximizing yield. Earnings have been positive in recent years. Due to the small size of ORL’s reserves, any increase in claims or mortality could cause a material change to its earnings, but should not materially impact ORI. Premiums have declined over the past several years, as the closed-term block premiums run off, and the occupational accident premiums trend lower. The company’s business profile consists of a closed block of term life insurance and the actively marketed occupational accident line. Despite its modest size, ORL is important strategically to the Old Republic organization.

The ratings of Old Republic Canada reflect its balance sheet strength, which AM Best assesses as very strong, as well as its adequate operating performance, neutral business profile and appropriate ERM. The ratings of Old Republic Canada also reflect its strategic importance within the Old Republic enterprise.

The ratings of Old Republic Canada recognize the synergies it gains as an affiliate of Great West Casualty Company, as well as its accident and sickness business. Partially offsetting these positive rating factors are the company’s limited product offering and challenging market environment in Canada.

The FSR of A+ (Superior) and the Long-Term ICRs of “aa-” (Superior) have been affirmed, with stable outlooks, for the following members of the Old Republic Insurance Companies:

BITCO General Insurance Corporation

BITCO National Insurance Company

Great West Casualty Company

Manufacturers Alliance Insurance Company

Old Republic General Insurance Corporation

Old Republic Insurance Company

Old Republic Surety Company

Old Republic Union Insurance Company

Pennsylvania Manufacturers Indemnity Company

Pennsylvania Manufacturers’ Association Insurance Company

This press release relates to Credit Ratings that have been published on AM Best’s website. For all rating information relating to the release and pertinent disclosures, including details of the office responsible for issuing each of the individual ratings referenced in this release, please see AM Best’s Recent Rating Activity web page. For additional information regarding the use and limitations of Credit Rating opinions, please view Guide to Best’s Credit Ratings. For information on the proper use of Best’s Credit Ratings, Best’s Performance Assessments, Best’s Preliminary Credit Assessments and AM Best press releases, please view Guide to Proper Use of Best’s Ratings & Assessments.

AM Best is a global credit rating agency, news publisher and data analytics provider specializing in the insurance industry. Headquartered in the United States, the company does business in over 100 countries with regional offices in London, Amsterdam, Dubai, Hong Kong, Singapore and Mexico City. For more information, visit www.ambest.com.

The U.S. Department of Labor’s proposal to rescind current guidance determining independent contractor status under the Fair Labor Standards Act will significantly benefit independent insurance agents and brokers and the consumers who rely on them for financial and risk-protection products and services. The current guidance is far too likely to misclassify independent contractors in the insurance space as employees. NAIFA supports DOL’s proposal to replace the current guidance “with guidance that is substantially similar to the guidance DOL adopted in 2021,” NAIFA President Christopher Gandy wrote in a letter to Andrew Rogers, administrator of the DOL’s Wage and Hour Division.

That earlier guidance, commonly known as the “Economic Realities Test,” determines a worker’s status based on the degree of their control over their work, their opportunities for profit or loss, the amount of skill required to perform the work, the permanence of the relationship between the worker and employer, and whether the work is part of an integrated unit of production. The current guidance uses a very broad definition of “economic dependence” to classify many independent business owners as employees. Under the Economic Realities Test, independent insurance and financial professionals are much more likely to be properly classified as contractors.

Misclassification can severely inhibit the success of professionals and their ability to serve the best interests of their clients. The majority of NAIFA’s members – insurance producers, broker dealer representatives, and/or independent registered investment advisors – are independent contractors who provide vital financial benefits and insurance services to consumers across the country. They are skilled practitioners who are licensed, highly trained, and tightly regulated. Many of them are entrepreneurs and small business owners who maintain their own offices, purchase their own business insurance, and hire their own employees. Their independent-contractor status allows them to focus on the needs of their clients and employees, have flexibility in their business models, and maintain control over the types of financial products they recommend and sell. A survey of NAIFA members found that more than 95% of those who were independent contractors under the 2021 rule desired to maintain that status.

“Independent insurance producers and independent financial advisors are vital to ensuring that millions of Americans have access to important financial benefits,” Gandy wrote to Administrator Rogers. “These professionals are deeply rooted in their communities and are best positioned to understand the needs of consumers. Ensuring their proper classification as independent contractors is to ensure the availability of products they can provide their clients.”

BELLEVUE, Wash.–(BUSINESS WIRE)–

Symetra today announced the promotion of Nicholas Mocciolo to chief investment officer, Symetra Financial Corporation. Mr. Mocciolo, interim co-president and senior managing director of Symetra Investment Management (SIM), has responsibility for the day-to-day management of the general account portfolios of Symetra Life Insurance Company and its affiliates. He reports to Tommie Brooks, executive vice president and chief financial officer of Symetra Financial Corporation.

Nicholas Mocciolo has been promoted to chief investment officer for Symetra Financial Corporation. Mr. Mocciolo is interim co-president and senior managing director of Symetra Investment Management.

SIM, a registered investment adviser, currently manages over $88 billion for affiliated Symetra Financial and Sumitomo Life accounts.

Mr. Mocciolo joined Symetra in January 2015 from White Mountains Advisors, LLC, where he led the derivatives sector and participated in Symetra general account portfolio management. Prior to White Mountains, Mr. Mocciolo was senior vice president, senior portfolio manager, derivatives, at Hartford Investment Management Company, where he was responsible for The Hartford’s enterprise-wide derivatives hedging activities.

“Nick has played a critical role in helping lead, manage and expand Symetra’s asset management capabilities, and was instrumental in the launch of SIM in 2019. He brings exceptional talent, investment knowledge, and management experience to his Symetra CIO role,” said Symetra Financial CFO Tommie Brooks. “Nick is also a trusted counselor to Symetra’s parent, Sumitomo Life, and has built a strong relationship with its investment management team over the last five years as SIM has overseen an increasingly larger portion of Sumitomo Life’s U.S.-based investment portfolio.”

Mr. Mocciolo received a bachelor’s degree in mathematics and a master’s degree in applied mathematics from the University of Connecticut and also earned a master’s degree in operations research from Columbia University. He is a Fellow of the Society of Actuaries (FSA) and has earned the Financial Risk Manager (FRM) designation.

About Symetra

Symetra Financial Corporation is a diversified financial services company based in Bellevue, Washington. In business since 1957, Symetra provides employee benefits, annuities and life insurance through a national network of benefit consultants, financial institutions, and independent financial professionals and insurance producers. For more information, visit www.symetra.com.

About Symetra Investment Management

Symetra Investment Management Company (SIM) is a Registered Investment Adviser offering discretionary investment advisory services to institutional clients. Founded in 2019 and headquartered in Farmington, Conn., SIM manages approximately $88.7 billion in assets across Investment Grade Corporate Credit, High Yield, Bank Loans, Commercial Mortgage Loans, Private Placements, Structured Credit, Hedging and Alternatives.

SIM and its subsidiary, Symetra Investment Management Real Estate Investors (SIM REI), have approximately 150 employees. SIM is a wholly owned subsidiary of Symetra Financial Corporation.